Opening a clinic requires Rs 30-75 lakhs investment, 18-24 months of negative cash flow, and carries the risk of failure — but offers an income ceiling of Rs 1-3 crore/year with full autonomy. Joining a corporate hospital requires zero investment and zero risk, with immediate Rs 2-5 lakhs/month salary — but caps your income at Rs 5-8 lakhs/month and ties your clinical decisions to EBITDA targets. The right choice depends on your capital, risk tolerance, specialty, and how much you value autonomy. Here's the honest financial comparison.

How Does the Financial Comparison Look Side by Side?

The two paths have fundamentally different risk-reward profiles. Upfront investment | Rs 30-75 lakhs (small), Rs 1-2.5 crore (specialty) | Rs 0 Monthly income (Year 1) | -Rs 1-2 lakhs (loss) | Rs 2-5 lakhs (guaranteed) Monthly income (Year 3) | Rs 2-5 lakhs (if successful) | Rs 3-6 lakhs Monthly income (Year 5+) | Rs 5-15 lakhs (if established) | Rs 4-8 lakhs (capped) Income ceiling | Functionally unlimited | Limited by salary bands + incentives Break-even timeline | 18-36 months | Immediate Risk of total loss | Real (30% of clinics fail in 3 years) | Near zero Clinical autonomy | Complete | Limited by hospital protocols Schedule control | You decide | Hospital decides Patient ownership | You own the relationship | Hospital owns the relationship Exit value | Clinic has sellable value | Nothing to sell Work-life boundary | You're always on call | Structured (somewhat)

What Does the Clinic Path Offer — Higher Ceiling but Higher Risk?

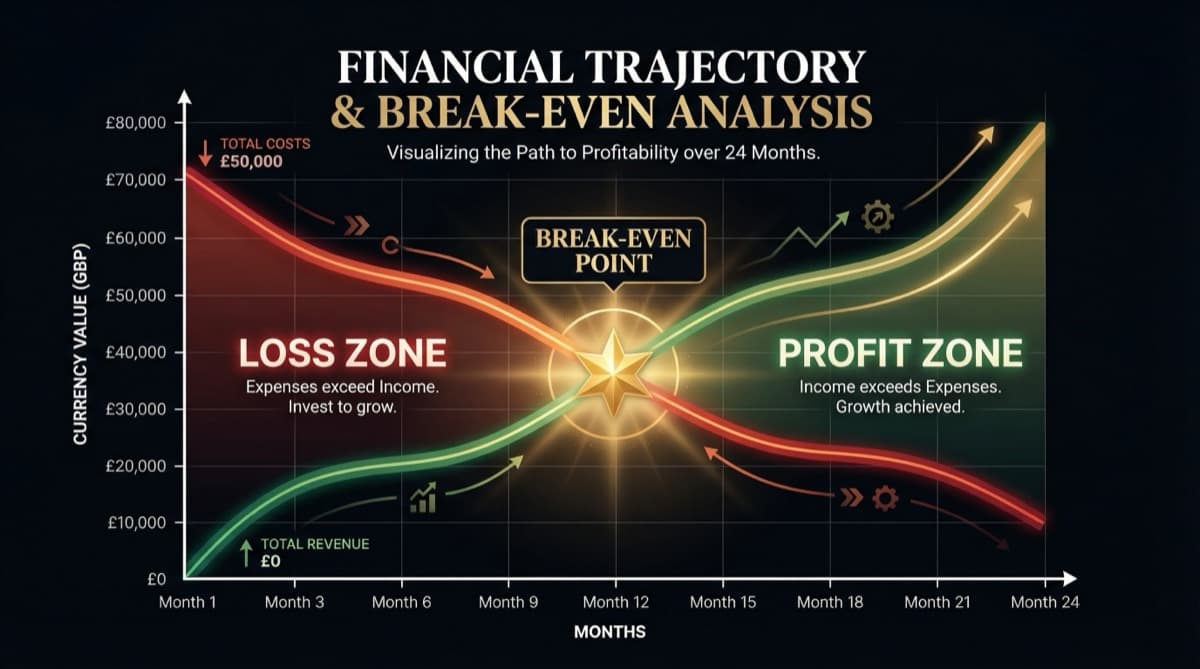

The financial trajectory unfolds over five years. The 5-Year Financial Model

Year 1 (Setup + Survival):

- Investment: Rs 30-50 lakhs

- Revenue: Rs 50K-3L/month (building)

- Costs: Rs 1.5-3L/month (fixed)

- Net: Rs -1 to -2 lakhs/month

- Cash burn: Rs 12-24 lakhs

Year 2 (Growth):

- Revenue: Rs 2-5L/month

- Costs: Rs 2-3.5L/month

- Net: Rs 0 to +1.5L/month

- Status: Break-even zone

Year 3 (Establishment):

- Revenue: Rs 4-8L/month

- Costs: Rs 2.5-4L/month

- Net: Rs 1.5-4L/month

- Status: Profitable

Year 5 (Mature Practice):

- Revenue: Rs 8-20L/month

- Costs: Rs 3-6L/month

- Net: Rs 5-14L/month

- Status: Strong returns

Total 5-year investment (including cash burn): Rs 50-80 lakhs Total 5-year net income: Rs 40 lakhs-1.5 crore (cumulative) Year 5 annual income: Rs 60 lakhs-1.7 crore

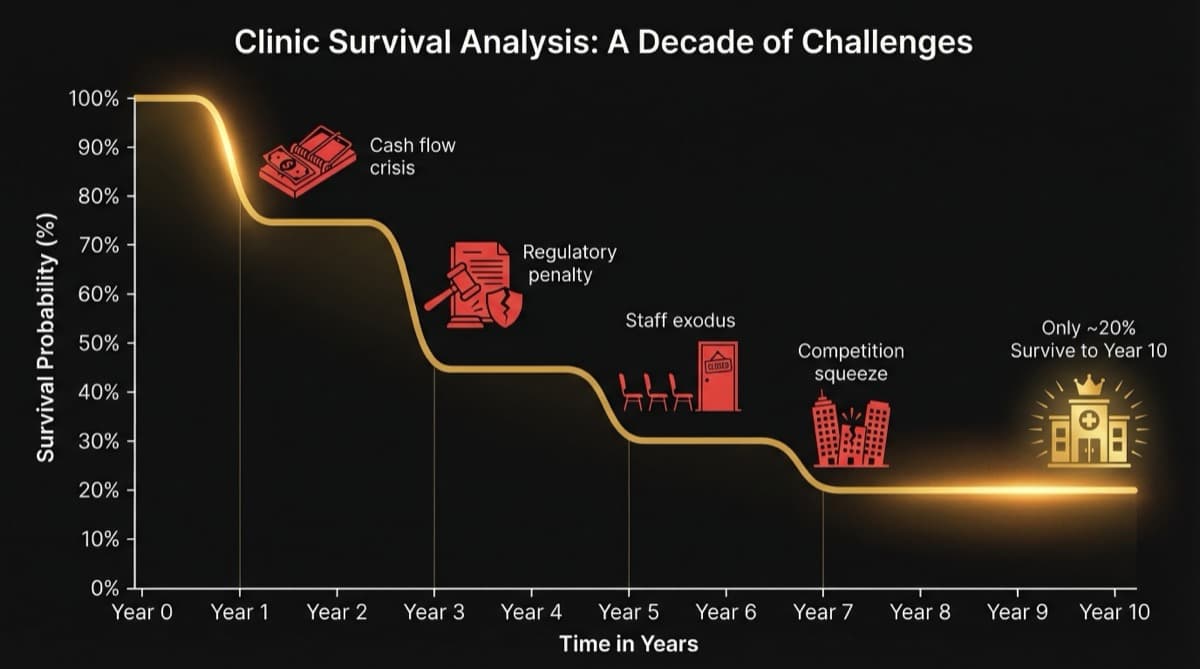

Why Clinics Fail

The 30% failure rate in the first 3 years follows predictable patterns:

- Rent-to-revenue ratio above 30% — location was too expensive for the patient catchment

- Undercapitalization — insufficient working capital to survive 18-month cash flow gap

- Wrong location — low footfall, poor visibility, no parking, competitor saturation

- EMI timing mismatch — equipment EMIs start before revenue justifies the investment

- No differentiation — in a market with 50 dermatology clinics per square kilometer, why would patients choose yours?

What Does the Corporate Hospital Path Offer — Lower Ceiling but Zero Risk?

The financial stability is immediate. The 5-Year Financial Model

Year 1:

- Salary: Rs 2-4L/month (junior consultant)

- Investment: Rs 0

- Net: Rs 2-4L/month from day one

Year 2:

- Salary: Rs 2.5-4.5L/month

- Performance bonuses: Rs 50K-1L/quarter

Year 3:

- Salary: Rs 3-5L/month

- Some revenue-share if negotiated

Year 5:

- Salary: Rs 4-8L/month

- Total compensation: Rs 50-100 LPA

Total 5-year income: Rs 1.2-3 crore (cumulative) Year 5 annual income: Rs 50 lakhs-1 crore

The Golden Handcuffs Problem

Corporate hospitals offer enough to live well but not enough to build wealth at the rate an independent practice can. The "golden handcuffs" effect: your salary is comfortable enough that the risk of leaving for independent practice feels irrational — even though the long-term ceiling is higher outside.

Additionally, PE-backed hospitals are structurally replacing revenue-share with fixed-plus-incentive models that cap your upside. The trend line for corporate hospital doctor income is flat or declining in real terms, not growing.

What Decision Framework Should You Use to Choose?

Your choice depends on your specific circumstances. Choose Clinic If:

- You have Rs 50-80 lakhs in accessible capital (savings, family support, or low-interest financing)

- Your specialty has strong self-pay patient demand (dermatology, ophthalmology, dental, orthopedics)

- You have an existing patient base (referral network, personal brand, community connections)

- You value autonomy over security

- You're willing to accept 18-24 months of financial stress

- You have a spouse/partner with stable income during the build phase

Choose Corporate Hospital If:

- You're carrying significant educational debt (Rs 40+ lakhs)

- Your specialty is primarily insurance/hospital-dependent (cardiology, oncology, critical care)

- You don't have startup capital or risk tolerance

- You want predictable income while building credentials

- You're in the first 3-5 years post-PG and still establishing clinical expertise

- You value structured hours over schedule flexibility

The Hybrid Path

Many successful doctors do both — sequentially:

Phase 1 (Age 30-35): Join a corporate hospital. Build clinical skills, reputation, and patient relationships on the hospital's dime. Save aggressively.

Phase 2 (Age 35-40): Open a clinic (evenings/weekends) while maintaining hospital affiliation. Test demand with minimal risk.

Phase 3 (Age 40+): Transition to full-time independent practice once patient volume supports it. The hospital served as a launchpad, not a destination.

Frequently Asked Questions

Is it better to open a clinic or work in a hospital? Neither is universally better. Clinic ownership offers higher income ceiling (Rs 1-3 crore/year), full autonomy, and asset value — but requires Rs 30-75 lakhs investment and 18 months of losses. Corporate hospital employment offers immediate Rs 2-5 lakhs/month with zero risk — but caps income and autonomy. Choose based on your capital, risk tolerance, and specialty.

How long does it take for a clinic to break even? Typically 18-36 months. Factors that accelerate break-even: procedure-heavy specialty, high footfall location, existing patient base, low rent, and strong referral network. Factors that delay it: rent-heavy location, consultation-only model, new market with no existing patients.

What percentage of clinics fail? Approximately 25-30% of new clinics fail within the first 3 years. Primary causes: undercapitalization, unfavorable rent-to-revenue ratio, poor location choice, and insufficient patient volume during the build phase.

Can I open a clinic with Rs 10-15 lakhs? A basic consultation-only clinic (no major equipment, small space, one staff member) can be started at Rs 10-15 lakhs. However, you'll need additional working capital of Rs 10-15 lakhs to survive the cash flow gap. Budget Rs 25-30 lakhs minimum for a clinic that can sustain its first 18 months.

Should I take a loan to open a clinic? Only if the loan terms are favorable (below 12% interest, 5+ year term) and you have a clear break-even plan. Avoid high-interest personal loans. Business loans at 10-12% are manageable if your specialty has strong revenue potential. Never borrow more than you can service from alternative employment income if the clinic fails.

Planning to launch your clinic? A strong brand identity is your foundation. See our Brand Sprint package at futurise.studio/services or view our portfolio at futurise.studio/portfolio