On this page

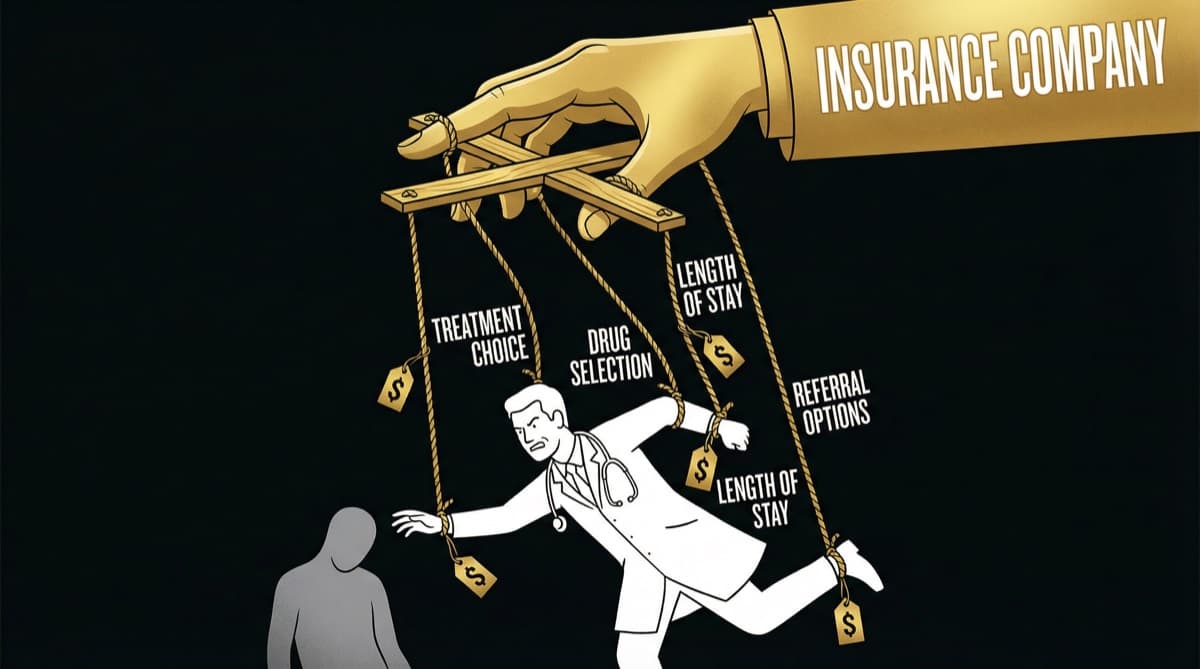

CGHS (Central Government Health Scheme) pays 3-4x more than PMJAY for the same procedure. A cataract surgery reimbursed at Rs 6,500 under PMJAY gets Rs 18,000-22,000 under CGHS. Private insurance falls between the two but varies widely. For your practice economics, the insurance mix matters more than clinical skill — same procedure, vastly different revenue depending on which insurer covers the patient.

The Reimbursement Rate Hierarchy

India has fragmented insurance. Depending on which scheme covers your patient, you get paid completely different amounts for identical work.

Comparative reimbursement rates (same procedures, different insurers):

Cataract surgery: PMJAY Rs 6,500 / Private Ins Rs 12,000 / CGHS Rs 20,000 — 3.1x difference. Appendicectomy: PMJAY Rs 15,000 / Private Ins Rs 22,000 / CGHS Rs 40,000 — 2.7x difference. Normal delivery: PMJAY Rs 6,000 / Private Ins Rs 12,000 / CGHS Rs 18,000 — 3x difference. Cesarean section: PMJAY Rs 10,000 / Private Ins Rs 18,000 / CGHS Rs 30,000 — 3x difference. CABG (heart surgery): PMJAY Rs 90,000 / Private Ins Rs 1,50,000 / CGHS Rs 3,00,000 — 3.3x difference. Hysterectomy: PMJAY Rs 25,000 / Private Ins Rs 35,000 / CGHS Rs 70,000 — 2.8x difference. ICU care (per day): PMJAY Rs 4,000 / Private Ins Rs 8,000 / CGHS Rs 15,000 — 3.75x difference.

Same procedure. Same hospital. Same doctor. Same outcome. But if your patient has CGHS vs PMJAY, hospital revenue differs by 300%. This isn't medical — it's administrative.

Q.Why CGHS Pays So Much More?

CGHS is for federal government employees. It's been around since 1954. CGHS can afford high reimbursement rates because: beneficiary base is stable (not growing), claim volume is lower (not all employees use every year), budget is protected (part of federal employee benefits), and political cost of changing CGHS is high (federal employees vote and complain).

PMJAY, by contrast: is newest (launched 2018), has massive beneficiary base (55+ crore), has growing claim volume, has no political protection (poor people have less political voice), and can have rates cut without electoral consequence.

Q.How Should You Approach Understanding Private Insurance Reimbursement?

Private insurance is fragmented across 30+ insurers. Each sets own rates. Private insurance negotiates rates hospital-by-hospital. A prestigious hospital gets paid more than a smaller clinic for the same procedure. This creates perverse incentive: bigger hospitals get higher reimbursement for identical work. Market power determines payment, not clinical quality.

Q.What Is the Income Implication For Your Hospital?

Scenario A (60% CGHS, 20% private insurance, 20% PMJAY): Daily revenue approximately Rs 35-40 lakh. Monthly revenue Rs 10-12 crore. Profit margin 35-40%.

Scenario B (20% CGHS, 30% private insurance, 50% PMJAY): Daily revenue approximately Rs 20-24 lakh. Monthly revenue Rs 6-7 crore. Profit margin 10-15%.

Same hospital. Same doctors. Same procedures. Insurance mix determines whether you're profitable or in crisis.

Need help with this?

Our team specializes in healthcare branding. Get personalized advice in a free 15-minute call.

Book a free 15-minute callQ.What Is The Reimbursement Gap For You Personally?

Assume your hospital gives you 15% of claim recovery:

CGHS cataract: Hospital Gets Rs 20,000, You Get Rs 3,000, Time To Payment 30 days. Private insurance cataract: Hospital Gets Rs 12,000, You Get Rs 1,800, Time To Payment 45 days. PMJAY cataract: Hospital Gets Rs 6,500, You Get Rs 975, Time To Payment 180 days.

Same surgery. You make 3.1x more if patient has CGHS vs PMJAY. Over a month with 20 surgeries: All CGHS Rs 60,000. All PMJAY Rs 19,500. Mixed 50/50 Rs 39,750. Your income is determined by insurance mix, not clinical skill.

Q.Why Doctors Prefer Certain Insurance Types?

CGHS (Preferred): High reimbursement rates, fast payment (30 days), minimal claim rejections (2-5%), minimal pre-authorization hassle, predictable economics.

Private Insurance (Acceptable): Medium-high reimbursement, medium payment speed (45-60 days), moderate claim rejections (15-20%), pre-authorization required, somewhat predictable.

PMJAY (Avoided when possible): Low reimbursement rates, slow payment (120-180 days), high claim rejections (40-60% in some states), extensive pre-authorization, unpredictable.

Q.What Is the Structural Injustice?

The reimbursement hierarchy creates a two-tier system:

Tier 1 (High reimbursement): CGHS beneficiaries — 62 lakh federal employees. Get priority appointments, better doctor attention, faster procedures, shorter wait times.

Tier 2 (Low reimbursement): PMJAY beneficiaries — poorest 55+ crore people. Get deprioritized appointments, less attentive care, longer wait times, worse outcomes (not due to clinical skill, but system design).

You're not consciously creating this two-tier system. It's structural. The payment difference creates it automatically.

Frequently Asked Questions

Q: Should I discourage PMJAY patients because reimbursement is low?

A: No. But be honest about payment delays.

Q: Does higher reimbursement mean I should prefer CGHS patients?

A: Not should. But honestly, most doctors do prefer higher-reimbursement patients. The question is whether you act on that preference in clinical decision-making. Don't.

Q: Should my choice of hospital depend on insurance mix?

A: If you have choices, yes. A hospital with 60%+ CGHS will be more stable financially than one with 60%+ PMJAY.

futurise. builds premium healthcare brands in 48 hours. Learn more at futurise.studio