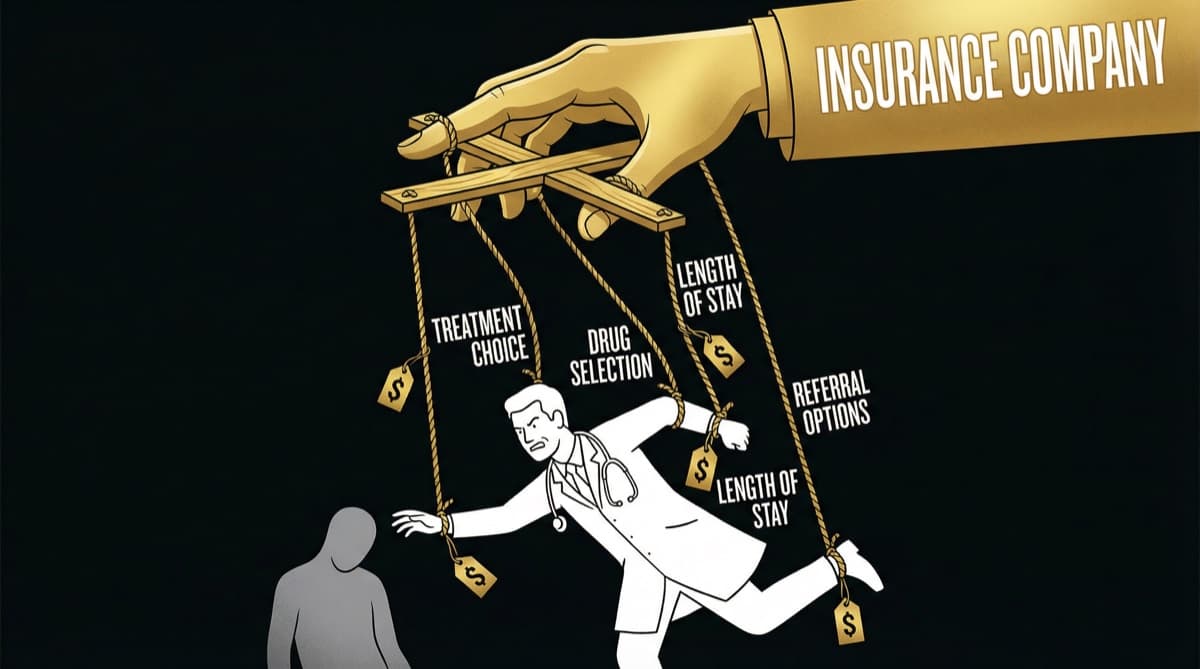

Insurance companies in India override clinical judgment daily through three structural mechanisms: pre-authorization requirements that delay or deny treatments, package rates that cap what procedures can cost, and claim rejections that punish doctors financially for clinical decisions the insurer disagrees with. In FY 2024-25, insurers rejected health claims worth Rs 30,000 crore — a 15% increase from the previous year. Every doctor practicing in India today operates within an invisible set of insurance-imposed constraints that most patients never see.

What Are the Three Mechanisms Insurance Companies Use to Control Treatment?

Insurance companies control clinical decisions through three structural mechanisms. 1. Pre-Authorization: The Permission Slip for Clinical Care

Before you can admit a patient for a planned procedure under cashless insurance, you need the insurer's approval. This is pre-authorization — and it gives the insurance company a veto over your clinical recommendation before you've even started treatment.

How it works in practice:

- You recommend a knee replacement for a 62-year-old patient with Grade 4 osteoarthritis

- Hospital submits pre-authorization request with clinical details to the insurer's TPA (Third Party Administrator)

- TPA medical officer (often a junior doctor reviewing files remotely) evaluates whether the procedure is "medically necessary"

- Approval, rejection, or request for additional documentation comes back in 24-72 hours

- If rejected, the patient either pays out of pocket or doesn't get the procedure

The structural problem: A TPA medical officer evaluating your pre-authorization request has never examined your patient, may not be a specialist in the relevant field, and is incentivized to control costs — not to optimize patient outcomes. Your 15 years of clinical experience gets overruled by a checklist.

Emergency loophole: Emergency admissions don't require pre-authorization, but insurers review them retrospectively. If the insurer decides post-facto that the admission "wasn't a genuine emergency," the claim gets rejected — and the hospital and doctor absorb the financial loss.

- 1Package Rates: The Price Ceiling on Your Medicine

Insurance companies (and government schemes like PMJAY) don't pay for individual services. They pay package rates — a fixed amount for a defined procedure regardless of what the actual clinical situation requires.

Example: Appendectomy

Surgeon fee | Rs 15,000-25,000 | — Anesthesia | Rs 8,000-12,000 | — OT charges | Rs 10,000-20,000 | — Room (3 days) | Rs 6,000-15,000 | — Consumables | Rs 5,000-10,000 | — Actual Total | Rs 44,000-82,000 | Package: Rs 25,000-40,000

When the package rate is lower than actual cost, the hospital absorbs the loss — or cuts corners. The surgeon's fee gets compressed first. The choice of consumables shifts to the cheapest available. The length of stay gets shortened to minimize costs.

The clinical impact: When a hip replacement package pays Rs 1.5 lakhs but the optimal implant costs Rs 1.2 lakhs alone, the doctor faces a choice: use a cheaper implant that fits the package, or use the better implant and have the hospital absorb the loss. Package rates don't just control costs — they influence clinical decisions.

- 1Claim Rejections: The Punishment After the Fact

Even after pre-authorization and treatment within package rates, claims can be rejected at the final settlement stage.

FY 2024-25 data: Insurers rejected health claims worth Rs 30,000 crore — a 15% jump from Rs 26,037 crore in FY 2023-24. This means roughly 1 in 5 claims faces some form of rejection or reduction.

Common rejection reasons that affect doctors:

- "Treatment not medically necessary" — insurer disagrees with your clinical judgment after the fact

- "Excluded procedure" — treatment you recommended falls outside policy coverage

- "Room rent sub-limit violation" — patient was in a room category that exceeds their policy limit, reducing the entire claim proportionally

- "Undisclosed pre-existing condition" — insurer discovers a condition the patient didn't declare (but you treated in good faith)

- "Insufficient documentation" — your clinical notes didn't meet the insurer's documentation standard

The doctor's financial exposure: In cashless treatment, when a claim is rejected, the hospital either absorbs the loss or attempts to recover from the patient. Either way, the doctor's revenue share or performance metrics take a hit. Repeated claim rejections make you a "high-cost" doctor in the hospital's analytics — which affects your contract renewal.

How Does Insurance Control Play Out in Your Daily Practice?

The impact is constant and pervasive. Morning OPD: You see a patient with suspected gallstones. You recommend laparoscopic cholecystectomy. Before you can schedule it, the hospital's insurance desk needs to check which insurer the patient has, what their package rate is for this procedure, and whether pre-authorization can be obtained. Your clinical recommendation waits for administrative clearance.

Afternoon surgery: You operate within the package rate constraints. The Rs 35,000 package means you use standard clips instead of the newer absorbable ones you prefer. The patient doesn't know the difference. Your clinical judgment was silently modified by a pricing model.

Evening paperwork: You complete discharge documentation knowing that insufficient detail will trigger a claim rejection. You spend 20 minutes on documentation that adds no clinical value but protects against insurer queries.

This cycle repeats daily. The cumulative effect: insurance logistics consume 15-25% of a doctor's administrative time, and financial constraints silently modify clinical decisions across millions of consultations per year.

What Is the IRDAI Framework — and What Are Regulators Doing?

IRDAI has introduced some protective measures:

- No rejection for want of documents (2024 regulation) — insurers can no longer reject claims solely for documentation gaps

- Standardized claim processing timelines — 30 days for non-investigation claims

- Cashless Everywhere directive — expanding cashless treatment access

But these address process, not structure. The fundamental mechanisms — pre-authorization vetoes, below-cost package rates, and retrospective claim denials — remain structurally intact.

Frequently Asked Questions

Do insurance companies actually override doctor recommendations? Not explicitly — they don't call you and say "don't do this surgery." Instead, they reject pre-authorization (preventing the surgery), set package rates below cost (forcing compromises on materials and technique), and reject claims after treatment (creating financial penalties for certain clinical decisions). The effect is the same as direct control, but through financial mechanisms rather than clinical instructions.

How much do claim rejections cost hospitals and doctors? Rs 30,000 crore in rejected claims in FY 2024-25 represents a massive financial burden on hospitals. For individual doctors, repeated claim rejections reduce revenue-share income and trigger administrative reviews. In PE-backed hospitals, doctors with high rejection rates face compensation consequences.

Can patients do anything about insurance controlling their treatment? Patients can choose top-up or super top-up policies that reduce package rate constraints, select hospitals outside cashless networks (and claim reimbursement), and understand their policy's room rent sub-limits before admission. The structural solution requires IRDAI to mandate reimbursement rates that reflect actual treatment costs.

Are government insurance schemes (PMJAY) better or worse than private insurance? PMJAY package rates are generally lower than private insurance, creating even greater cost pressure on hospitals. However, PMJAY covers a larger range of procedures (1,961 packages). The key difference: private insurance is a contractual relationship you can negotiate; PMJAY rates are government-set and non-negotiable.

What documentation protects doctors from claim rejections? Detailed clinical notes justifying medical necessity, documented informed consent, investigation reports supporting the diagnosis, and treatment rationale connecting diagnosis to procedure. The documentation burden is real — but it's the primary defense against retrospective claim denial.

futurise. builds premium healthcare brands in 48 hours. Learn more at futurise.studio