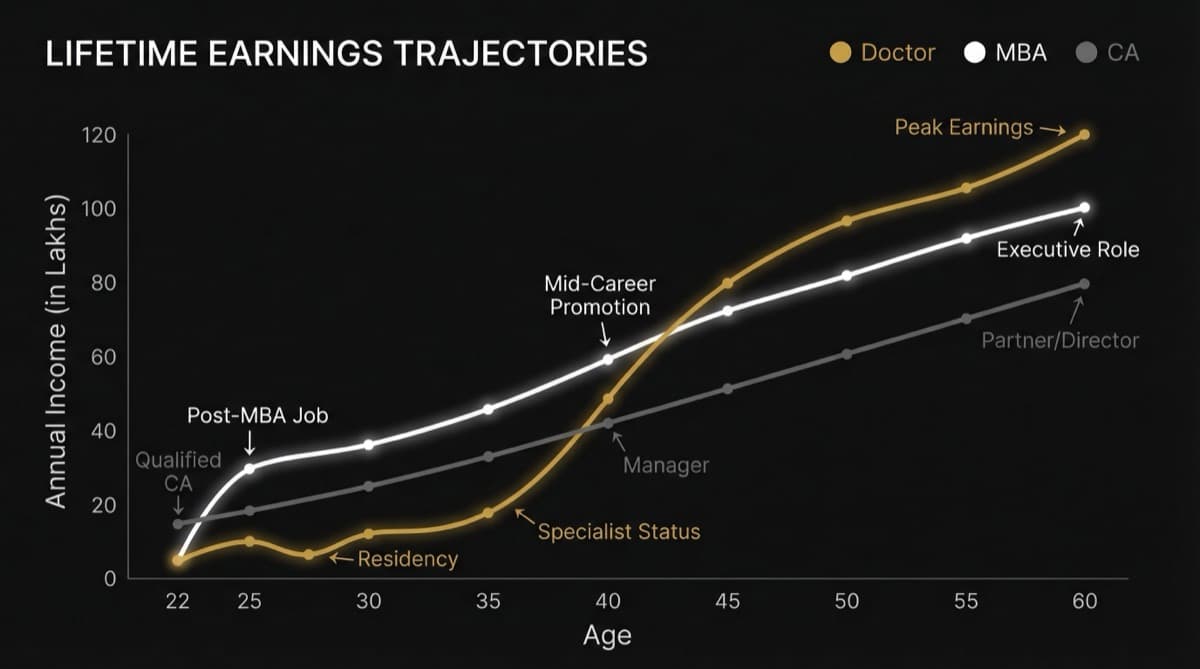

Most Indian doctors don't start earning meaningful income until age 30-32 — roughly 8-10 years after their MBA and CA peers hit Rs 15-25 LPA. An MBBS graduate exits medical college at 24, earns Rs 40-90K/month as a junior doctor, enters PG at 25-27, works as a resident at Rs 60-80K/month until 28-30, and only starts building a real income in their early 30s. Meanwhile, an MBA graduate from a Tier 1 B-school earns Rs 20-35 LPA by age 24 and an IIM peer has often accumulated Rs 1-2 crore in total earnings by the time the doctor writes their first real paycheck.

What Does the Doctor's Earning Timeline Look Like Year by Year?

Here is the full timeline from MBBS entry to peak earnings. 18-23 | MBBS (5.5 years) | Rs 0 (paying fees) | -Rs 3-25 lakhs/year (tuition) | MBA/CA peers: still in college 24 | Internship | Rs 15-30K (stipend) | Rs 2-4 LPA | MBA fresher: Rs 8-35 LPA 24-25 | Junior Resident / Job hunt | Rs 40-90K | Rs 5-10 LPA | CA fresher: Rs 8-12 LPA 25-28 | PG Residency (MD/MS) | Rs 50-80K (stipend) | Rs 6-10 LPA | MBA with 3 yrs exp: Rs 15-30 LPA 28-30 | Senior Resident / Fellowship | Rs 80K-1.5L | Rs 10-18 LPA | CA with 5 yrs: Rs 15-30 LPA 30-32 | Early Practice / Junior Consultant | Rs 1.5-3L | Rs 18-36 LPA | MBA mid-career: Rs 25-50 LPA 32-35 | Establishing Practice | Rs 2-5L | Rs 25-60 LPA | Crossover zone begins 35-40 | Established Specialist | Rs 3-8L | Rs 40-100 LPA | MBA senior: Rs 40-80 LPA 40-50 | Peak Earning Years | Rs 5-25L | Rs 60 LPA - 3 Cr | Doctor potentially overtakes peers

The structural insight: Doctors don't have a lower earning ceiling — they have a later earning start. The cumulative impact of this 8-10 year delay is enormous because those are the years of highest compounding for investments.

Why Is the Earning Delay Structural, Not Personal?

The delayed earning curve is not because doctors study slowly or make poor choices. It's engineered into the system.

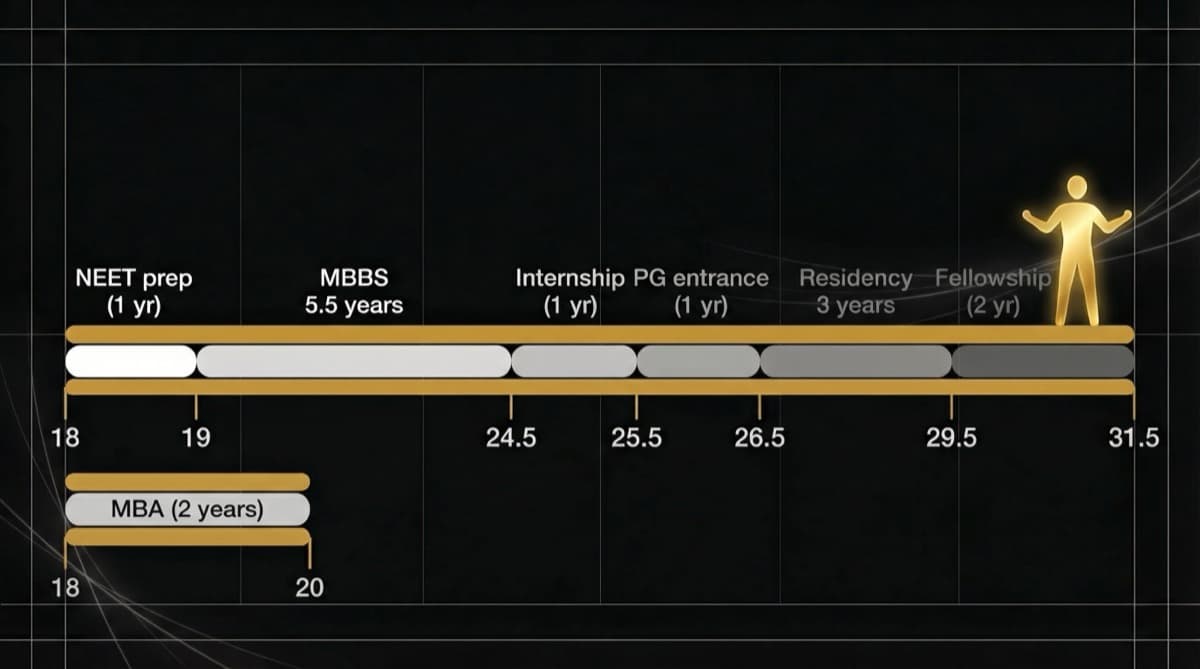

The Training Pipeline Is 10-15 Years Long

- MBBS: 5.5 years (the longest undergraduate degree in India)

- Internship: 1 year (mandatory, paid at stipend level)

- NEET PG preparation: 6 months - 2 years (most don't clear on the first attempt)

- PG (MD/MS): 3 years (paid at stipend level)

- Fellowship/Super-specialty (optional): 2-3 years

- Total time before independent practice: 10-15 years after entering medical college

An 18-year-old who enters MBBS is structurally committed to a decade or more of training before earning what their non-medical peers earned in year one of their careers.

The NEET PG Bottleneck Adds Years

India has 1,18,000 MBBS seats but approximately 65,000 PG seats. This means roughly 45% of MBBS graduates who want to specialize face at least one year of gap — and many face two or three. Each gap year is a year of no real income (or Rs 40-60K/month at best).

The NEET PG bottleneck is structural, not academic. It exists because medical education policy expanded MBBS seats far faster than PG seats. The result: lakhs of qualified MBBS doctors in a holding pattern, unable to specialize, earning below their potential.

Stipends During Training Are Below Market

Government PG stipends range from Rs 50,000-1,10,000/month depending on institution. At AIIMS and PGIMER, stipends are at the higher end with NPA and risk allowances. At state medical colleges, Rs 50-65K is common.

These amounts are not "training wages" in any meaningful sense. Residents working 100-120 hours per week at Rs 60K/month earn approximately Rs 125/hour — less than many skilled trades.

How Does the Compound Interest Problem Affect Doctors?

The earning delay creates a financial gap that goes beyond salary comparison. It's about compound interest.

Consider two individuals starting at age 24:

MBA graduate: Starts investing Rs 5 lakhs/year at age 24. By age 35, has invested Rs 55 lakhs with approximately Rs 90 lakhs accumulated (at 12% annual return). By age 45: approximately Rs 3.5 crore.

Doctor: Starts investing Rs 5 lakhs/year at age 32 (after PG completion and practice establishment). By age 35, has invested Rs 15 lakhs with approximately Rs 18 lakhs accumulated. By age 45: approximately Rs 1.2 crore.

The gap at age 45: Rs 2.3 crore — entirely due to the 8-year delay in starting investments, even with identical annual contributions thereafter.

This compound interest gap is why doctors who earn Rs 1 crore/year at age 45 may still have less net worth than MBA peers earning Rs 50 LPA — the MBA peer had two decades of compounding returns on investments that the doctor couldn't make during training.

When Do Different Medical Specialties Start Earning "Real Money"?

"Real money" is subjective, but let's define it as Rs 30+ LPA — enough to live comfortably, service any educational loans, and invest meaningfully.

General Medicine / Family Practice | 35-40 | Slower build, volume-dependent General Surgery | 33-38 | Practice building + reputation Orthopedics | 32-36 | Procedure-heavy, faster monetization Cardiology (DM) | 33-36 | Super-specialty premium + procedures Dermatology | 30-34 | OPD-heavy, cosmetic procedures accelerate income Radiology | 32-36 | Diagnostic volume-dependent Ophthalmology | 31-35 | Procedure-focused, LASIK/cataract clinics Oncology (DM/MCh) | 34-38 | Longer training, but high terminal income Psychiatry | 35-40+ | Lower procedure income, therapy-dependent Public Health / Community Medicine | 35-40+ | Government/NGO salary scales, slower growth

The fastest path to Rs 30+ LPA: Procedure-heavy specialties in metro cities with self-pay patients. Dermatology, ophthalmology, and orthopedics have the shortest time-to-income because procedures generate high per-unit revenue.

The slowest path: Non-procedural specialties (psychiatry, community medicine) and any specialty in Tier 2/3 cities where fee realization is 40-60% lower than metros.

What Should Parents of Medical Students Understand About Earnings?

If your child has entered MBBS, here's the financial reality:

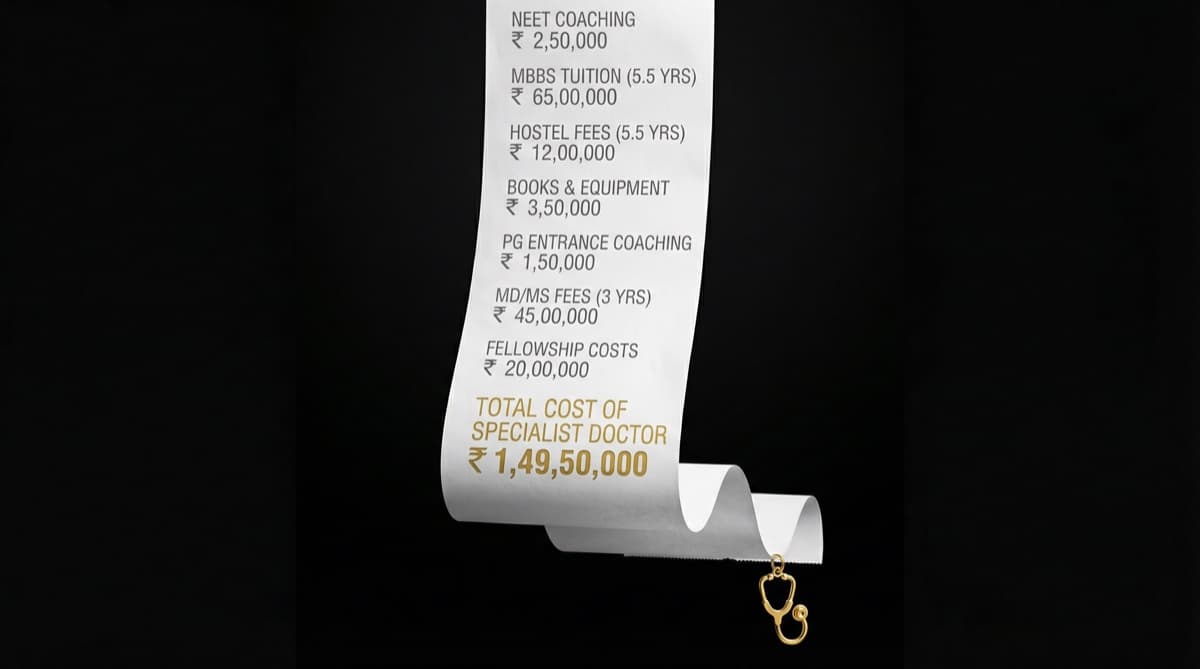

Ages 18-24: They are not "getting a degree." They are making a 10-15 year investment with no financial return for at least 6 years. Budget accordingly.

Ages 24-30: They will earn less than your neighbor's child who did MBA or CA. This is structural, not a reflection of their ability. Don't compare. Don't pressure.

Ages 30-35: They will begin earning well — if they've chosen the right specialty for their market and built patient relationships. This is the critical career-building phase. Support, don't interfere.

Ages 35+: If everything goes well, their earning potential exceeds most other professions. But "if everything goes well" depends on specialty choice, geography, practice model, and a bit of luck.

Frequently Asked Questions

When do MBBS doctors start earning in India? MBBS doctors begin earning during their internship year (age 23-24) at stipends of Rs 15,000-30,000/month. First "real" income (Rs 40-90K/month) comes when they join as junior doctors at age 24-25. Meaningful income (Rs 1.5-3 lakhs/month) typically begins only after PG completion at age 28-32.

Why are Indian doctor salaries so low initially? Two structural factors: supply (1,18,000 MBBS graduates annually competing for limited positions) and training classification (PG residents are classified as "trainees" despite providing critical clinical service, justifying below-market stipends). Starting salaries have remained at Rs 40-60K/month for a decade despite inflation.

Do doctors eventually earn more than engineers and MBAs? Top doctors (super-specialists in metro practice) earn Rs 1-3 crore annually — exceeding most engineering and MBA salaries. But the median doctor earns Rs 30-50 LPA, which is comparable to (not higher than) mid-senior MBA and engineering roles. The delayed start means cumulative lifetime earnings are often lower despite higher peak earnings.

Is it worth doing super-specialty (DM/MCh) despite the extra years? Financially: DM/MCh adds 3 years of training (at stipend-level income) but can double or triple your earning potential compared to MD/MS alone. A cardiologist (DM) earning Rs 80 LPA-2 crore versus a general physician at Rs 30-50 LPA makes the math clear. The trade-off is 3 additional years in the delayed-earning zone.

What's the best financial decision a young doctor can make? Start investing during residency — even Rs 5,000-10,000/month in SIPs. The 8-year delay in earning means every month of invested savings before age 30 has outsized impact due to compounding. This single habit can close the wealth gap with non-medical peers over a 30-year horizon.

futurise. builds premium healthcare brands in 48 hours. Learn more at futurise.studio