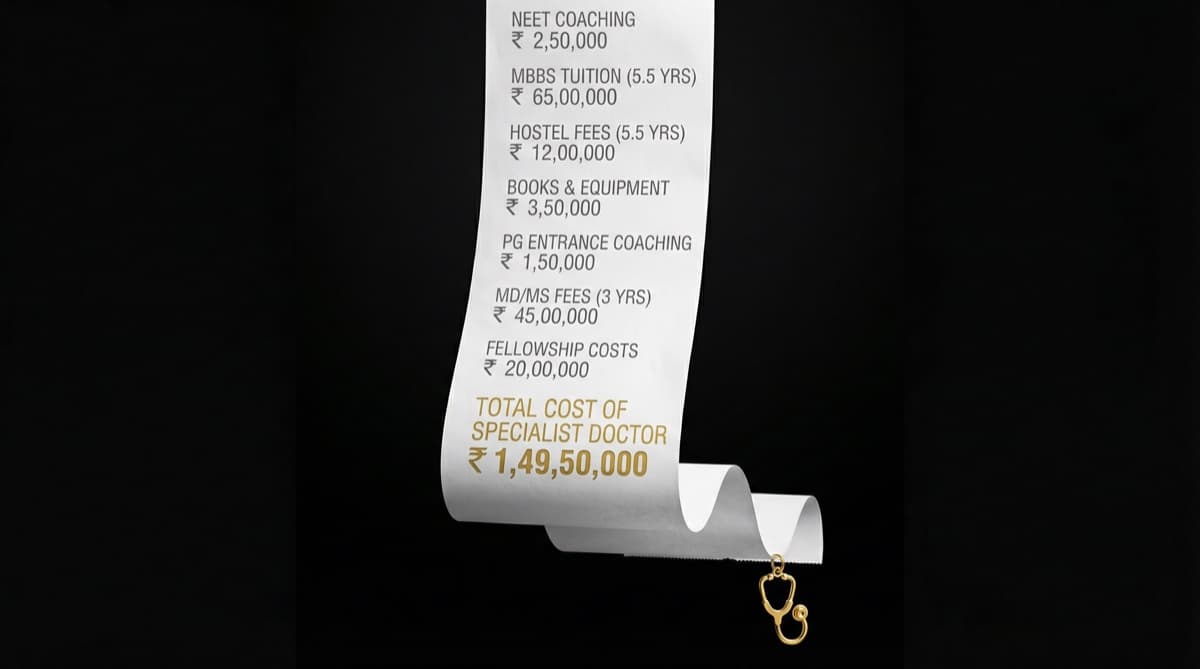

The total cost of becoming a specialist doctor in India ranges from Rs 50 lakhs (government college, all stages) to over Rs 2 crore (private college MBBS + private PG), when you include tuition, living expenses, and the opportunity cost of 10-15 years of forgone full-time income. The money you spend on fees is only half the story — the other half is the money you didn't earn while your non-medical peers accumulated salaries, investments, and career growth for a decade.

What Are the Direct Costs You Actually Pay to Become a Specialist?

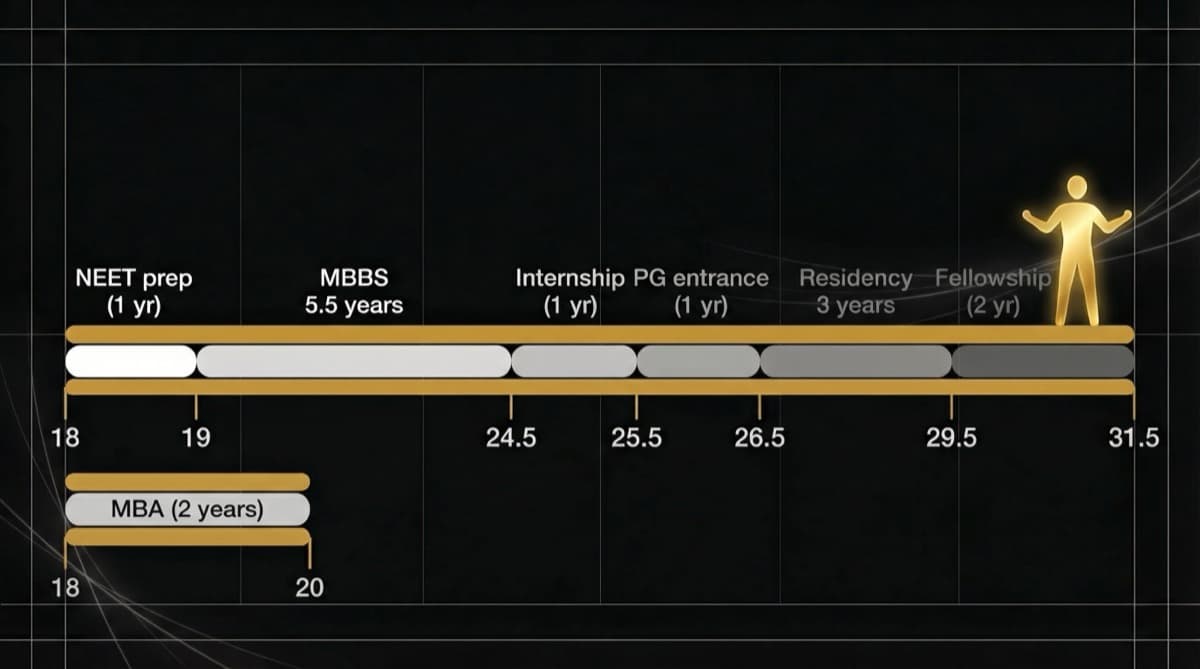

Direct costs vary dramatically by institution type. MBBS (5.5 Years)

Government (General Category) | Rs 10,000-1,00,000/year | Rs 50,000-5 lakhs | Heavily subsidized; most affordable path Government (Management/NRI Quota) | Rs 2-5 lakhs/year | Rs 10-25 lakhs | Higher fees for reserved seats Private Medical College | Rs 10-25 lakhs/year | Rs 55 lakhs-1.4 crore | Varies enormously by college and state Deemed University | Rs 15-30 lakhs/year | Rs 80 lakhs-1.65 crore | Often the most expensive Abroad (Russia, China, Philippines) | Rs 3-8 lakhs/year | Rs 20-50 lakhs | Lower fees but additional costs (FMG exam, adaptation)

The 50x cost gap is real: A student at a government medical college pays Rs 50,000/year. Their classmate at a private deemed university pays Rs 25 lakhs/year. They sit for the same exam, get the same degree, and compete for the same jobs. This is the most extreme cost disparity in any Indian professional education.

Postgraduate (MD/MS) — 3 Years

Government (General) | Rs 10,000-50,000/year | Rs 30,000-1.5 lakhs | Stipend: Rs 50-80K/month (covers living) Government (Management) | Rs 5-15 lakhs/year | Rs 15-45 lakhs | Stipend partially offsets Private Medical College | Rs 15-40 lakhs/year | Rs 45 lakhs-1.2 crore | Limited/no stipend in many private colleges DNB (Hospital-based) | Rs 2-10 lakhs/year | Rs 6-30 lakhs | Stipend: Rs 40-70K/month

Super-Specialty (DM/MCh) — 3 Years

Government | Rs 1-5 lakhs total | Rs 80K-1.1L/month Private | Rs 30-80 lakhs total | Variable

How Much Do Living Expenses Add During Medical Training?

Medical training doesn't happen in a vacuum. For 10-15 years, you need to eat, sleep, commute, and exist.

Hostel/Accommodation | Rs 5,000-15,000 | Rs 60K-1.8L | Rs 6-18 lakhs Food | Rs 5,000-10,000 | Rs 60K-1.2L | Rs 6-12 lakhs Books & Study Materials | Rs 1,000-3,000 | Rs 12K-36K | Rs 1.2-3.6 lakhs NEET Coaching (UG + PG) | — | Rs 1-5 lakhs per course | Rs 2-10 lakhs Transport / Miscellaneous | Rs 3,000-8,000 | Rs 36K-96K | Rs 3.6-9.6 lakhs Total Living Expenses | Rs 19-53 lakhs

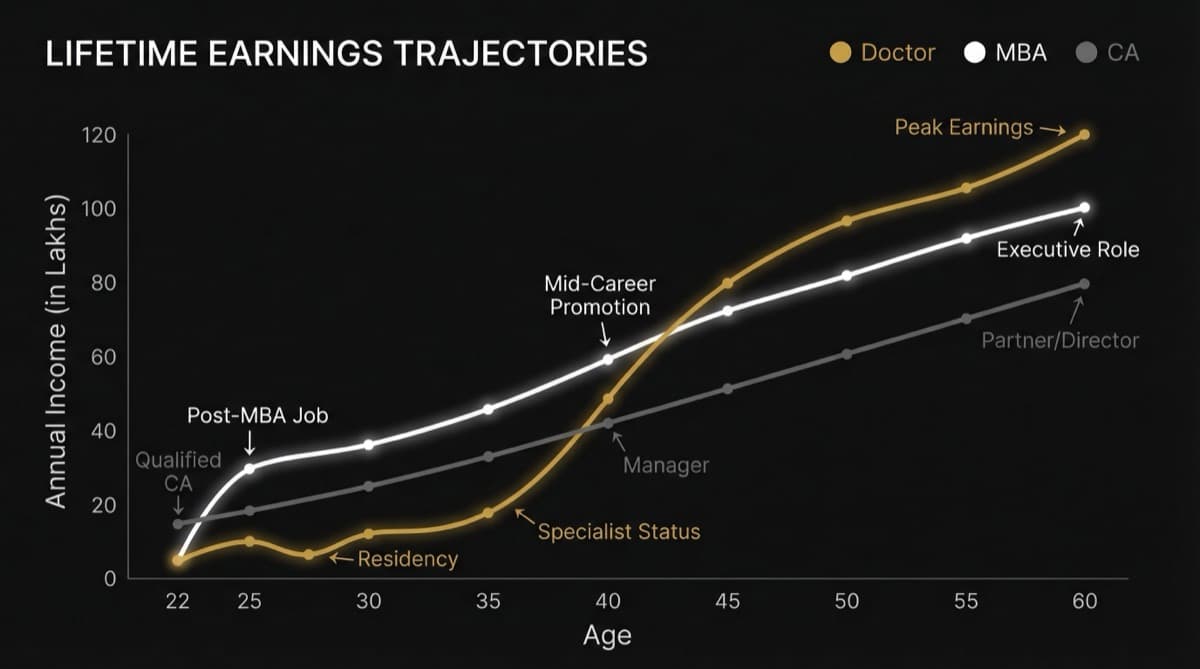

What Is the Opportunity Cost — the Invisible Expense — of Medical Training?

This is where the real cost hides. Opportunity cost is the income you forgo while studying and training instead of working.

Scenario comparison — Age 18 to 32:

Age 18-23 (MBBS) | Rs 0 (paying fees) | Rs 0 (also in college) | Rs 0 Age 24 (Internship) | Rs 2-4 LPA | Rs 8-15 LPA (first job) | Rs 6-11 LPA Age 25-27 (PG) | Rs 6-8 LPA (stipend) | Rs 12-25 LPA (3 yrs experience) | Rs 6-17 LPA Age 28-30 (SR/Fellowship) | Rs 10-15 LPA | Rs 18-35 LPA | Rs 8-20 LPA Age 30-32 (Early practice) | Rs 18-36 LPA | Rs 25-50 LPA | Rs 7-14 LPA Cumulative Gap | Rs 55 lakhs - 1.5 crore

The opportunity cost ranges from Rs 55 lakhs (conservative, comparing to average employment) to Rs 1.5 crore (comparing to a top MBA track). This is money that was never earned, never invested, and never compounded.

What Is the Total Investment When You See the Full Picture?

When you add everything up, the numbers are significant. MBBS Fees | Rs 50K-5 lakhs | Rs 55 lakhs-1.4 crore PG Fees | Rs 30K-1.5 lakhs | Rs 45 lakhs-1.2 crore Living Expenses (10 years) | Rs 19-30 lakhs | Rs 25-53 lakhs NEET Coaching (UG + PG) | Rs 2-5 lakhs | Rs 3-10 lakhs Opportunity Cost | Rs 55-80 lakhs | Rs 55 lakhs-1.5 crore TOTAL INVESTMENT | Rs 77 lakhs-1.2 crore | Rs 1.8-4.7 crore

The government medical college advantage is clear: Even including opportunity cost, the government path costs under Rs 1.2 crore. The private path can exceed Rs 4 crore — an amount that requires Rs 50+ LPA in sustained income just to generate a reasonable return on investment.

What Is the ROI Calculation for Each Medical Education Pathway?

Let's calculate whether the investment actually pays off, assuming a 35-year career earning period:

Government MBBS + Government PG (Best Case ROI)

- Total investment: Rs 80 lakhs - 1 crore

- Starting income at 30: Rs 18-30 LPA

- Peak income at 45: Rs 50 LPA - 2 crore

- Estimated lifetime earnings: Rs 10-25 crore

- ROI: Strong (10-25x investment)

Private MBBS + Private PG (Worst Case ROI)

- Total investment: Rs 3-4.7 crore

- Starting income at 30: Rs 18-30 LPA (same jobs as government grads)

- Peak income at 45: Rs 50 LPA - 2 crore (same ceiling)

- Estimated lifetime earnings: Rs 10-25 crore

- ROI: Moderate to Weak (2-8x investment)

The structural injustice: a private college doctor invests 3-5x more than a government college doctor but competes for the same positions, earns the same salaries, and has the same career ceiling. The extra investment buys the degree — not better career outcomes.

What Is the Debt Burden Reality for Medical Students?

Many private medical college students finance their education through loans.

Typical education loan for private MBBS:

- Loan amount: Rs 40-80 lakhs

- Interest rate: 8-12% per annum

- Repayment period: 10-15 years

- Monthly EMI (on Rs 60 lakh loan at 10%): Rs 79,000/month

The timing problem: Loan repayment typically begins during residency, when income is Rs 50-80K/month as a PG stipend. The EMI alone can exceed the stipend. Many residents rely on family support or defer payments (at accumulating interest) during training.

By the time the doctor starts earning at age 30, their Rs 60 lakh loan has grown to Rs 80-90 lakhs with accumulated interest. This debt load limits the doctor's ability to invest, build savings, or take career risks (like opening a practice) during the critical early-career phase.

Frequently Asked Questions

What is the cheapest way to become a specialist doctor in India? Government medical college (MBBS) followed by government PG — total direct cost of Rs 2-7 lakhs over 8.5 years. The catch: you need a high NEET rank, which typically requires Rs 2-5 lakhs in coaching. Still, the total cost is Rs 5-12 lakhs versus Rs 1-3 crore at a private institution.

Is private medical college worth the investment? Purely on financial ROI: usually no. A private MBBS costing Rs 1 crore leads to the same job market as a government MBBS costing Rs 3 lakhs. The private college is only "worth it" if the alternative is not becoming a doctor at all — and if the student has realistic expectations about the debt burden.

How much should parents save for their child's medical education? If targeting private medical college: Rs 1-1.5 crore for MBBS alone (fees + living expenses). If targeting government: Rs 10-20 lakhs total (including coaching and living expenses). Start a dedicated education fund early — the power of compounding over 15-17 years before MBBS entry is the best financial strategy for medical education.

Can doctors recover the investment from private medical college? Yes, but it takes time. A specialist earning Rs 40-80 LPA will mathematically recover a Rs 2-3 crore investment over 10-15 years of practice. A super-specialist earning Rs 1 crore+ recovers it faster. A general practitioner earning Rs 15-25 LPA may take 20+ years — by which point the inflation-adjusted ROI is marginal.

Why don't more students choose government medical colleges? They all want to — but there aren't enough seats. Government medical colleges have approximately 47,000 MBBS seats (out of 1,18,000 total). Competition is intense: top 40% NEET scores go to government colleges, the rest either pay for private education or pursue other careers. The constraint is seat availability, not student preference.

futurise. builds premium healthcare brands in 48 hours. Learn more at futurise.studio