On this page

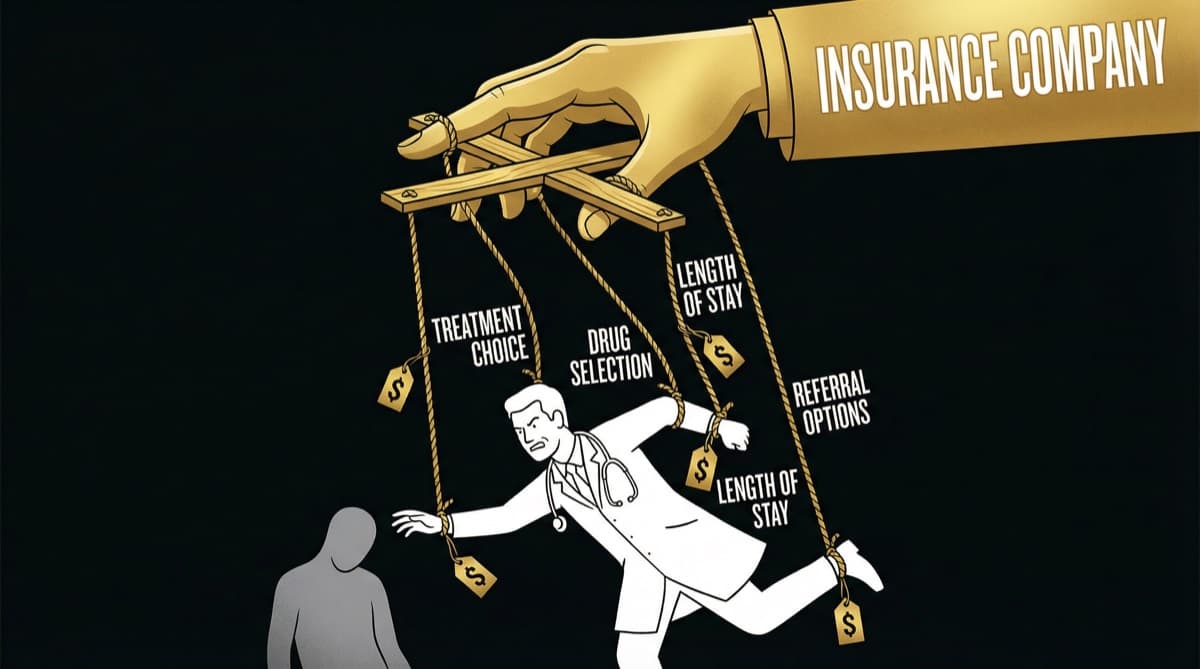

Government schemes hurt private hospitals structurally. PMJAY reimbursement is 40-60% below private hospital costs, forcing hospitals to cross-subsidize — charge private patients 2-3x more to offset government scheme losses. This makes private healthcare unaffordable, which then justifies more government scheme expansion, which forces hospitals deeper into losses. It's a destructive cycle with no equilibrium.

The Economics: How PMJAY Destroys Private Hospital Margins

Case Study: 100-Bed Hospital in Bangalore. 100 beds, 70% occupancy = 70 daily admissions. 30% PMJAY, 50% private, 20% CGHS. Average length of stay: 3 days. Patient turnover: 23 patients per day.

Total cost per patient per day: Rs 18,000-24,000 (including doctor's fee, nursing staff, room maintenance, medications, diagnostics, administrative overhead).

Revenue per patient: PMJAY Rs 4,000 (80% loss per day). Private Rs 12,000-15,000 (40-50% margin). CGHS Rs 15,000 (35-40% margin).

Daily hospital financials: 7 PMJAY patients -Rs 98,000 to -140,000. 12 private patients +Rs 60,000 to +96,000. 4 CGHS patients +Rs 24,000 to +36,000. Net daily: -Rs 14,000 to -8,000 (LOSS). This hospital is unprofitable by design.

Q.What Is The Cross-Subsidy Trap?

Hospital needs 10% profit margin to survive. With 30% PMJAY patients: PMJAY brings Rs 30 revenue but costs Rs 50 (net -Rs 20). Private patients must generate Rs 50 profit for hospital to net Rs 10. If private patient costs Rs 30 to treat, hospital charges Rs 50-60.

Private patient subsidizes hospital's PMJAY losses. This is called cross-subsidy.

The Price Multiplier Effect: Appendicectomy true cost Rs 25,000, PMJAY pays Rs 15,000, shortfall Rs 10,000, markup needed 40%, private price Rs 35,000. Cesarean section true cost Rs 22,000, PMJAY pays Rs 10,000, shortfall Rs 12,000, markup needed 55%, private price Rs 35,000.

Private patients pay 37-55% MORE than true cost due to government scheme cross-subsidy. This makes private healthcare expensive for middle-class patients who can't afford private rates but don't qualify for government schemes.

Q.What Is Feedback Loop: A Destructive Spiral?

- 1Government launches PMJAY to provide coverage.

- 2Private hospitals initially accept it.

- 3Hospitals discover PMJAY reimbursement is below cost.

- 4Hospitals raise private prices to cross-subsidize PMJAY.

- 5Private healthcare becomes unaffordable for middle class.

- 6Middle class pushes back, demands more government coverage.

- 7Government expands scheme (same reimbursement rates).

- 8Hospitals raise private prices further.

- 9Healthcare becomes even more unaffordable.

- 10Hospitals start exiting schemes, reducing bed capacity.

- 11Government scheme patients have fewer beds, longer waits.

- 12Government considers more control/regulation.

- 13Regulations make hospitals less profitable, more hospitals exit.

- 14Death spiral.

We're currently at step 11-12.

Q.What Is Hospital Exits From PMJAY?

PMJAY Hospital Empanelment Trend: 2018-2019 5,000+ new hospitals (massive expansion). 2019-2020 4,500+ (continued). 2020-2021 2,000+ (slower growth). 2021-2022 1,500+ (declining). 2022-2023 800+ (sharp decline). 2023-2024 316/month (very low). 2024-2025 111/month (collapsing).

Need help with this?

Our team specializes in healthcare branding. Get personalized advice in a free 15-minute call.

Book a free 15-minute callQ.What Would Fix This?

Option 1: Index reimbursement to inflation. Update PMJAY rates annually. Hospital economics become sustainable.

Option 2: Tiered reimbursement by hospital quality. Pay premium hospitals more. Incentivizes quality improvement.

Option 3: Government directly funds gap. Reimburse 100% of cost. Sustainable volume, affordable private healthcare.

Option 4: Reduce scope of scheme. Focus on 500 packages for poorest 10 crore. Concentrate resources.

None of these are being done. Instead, government is maintaining current policy and hoping hospitals somehow absorb losses.

Frequently Asked Questions

Q: If hospitals are losing money on government schemes, why do they keep them?

A: Regulatory requirement in many states. Hospitals need some government scheme beds to get licenses, land permits, tax breaks.

Q: What should doctors do if their hospital is losing money?

A: Ask administration for financial transparency. If hospital is unsustainable, your salary and job are at risk. Push for either increasing private patient volume or exiting government schemes.

futurise. builds premium healthcare brands in 48 hours. Learn more at futurise.studio