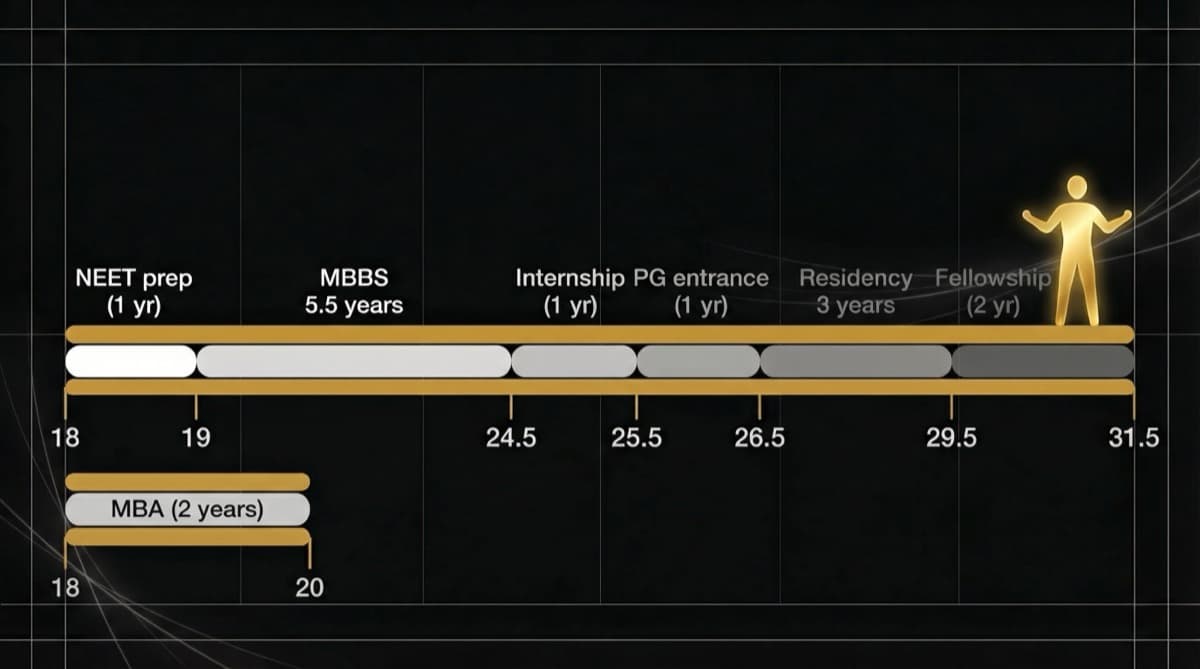

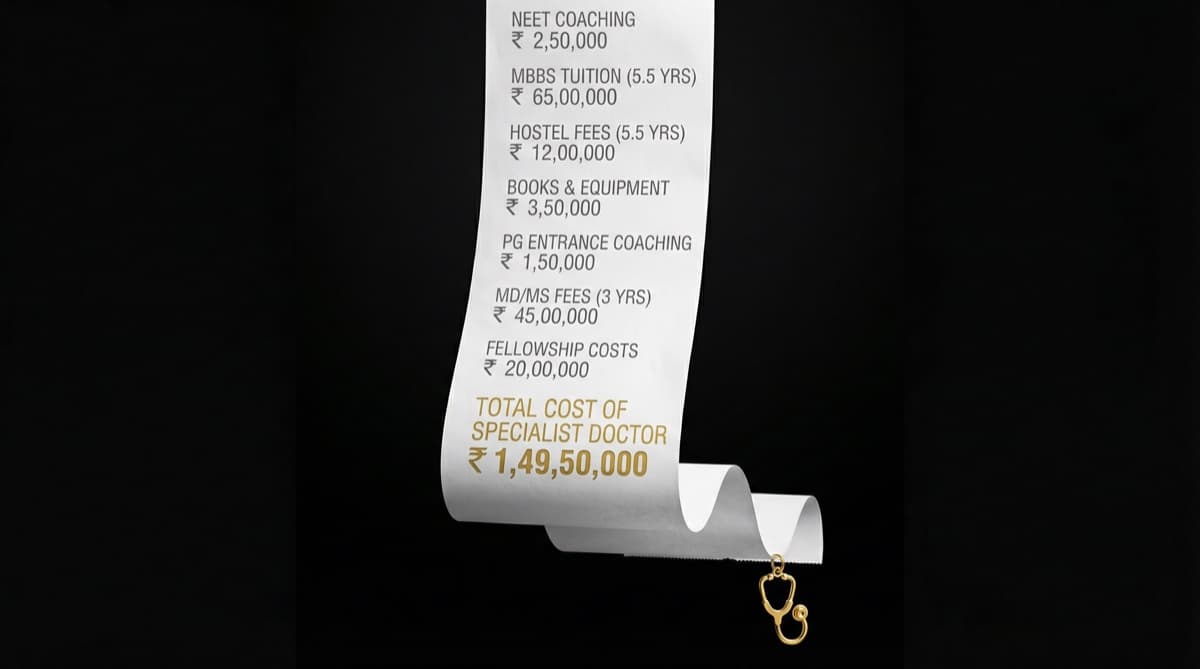

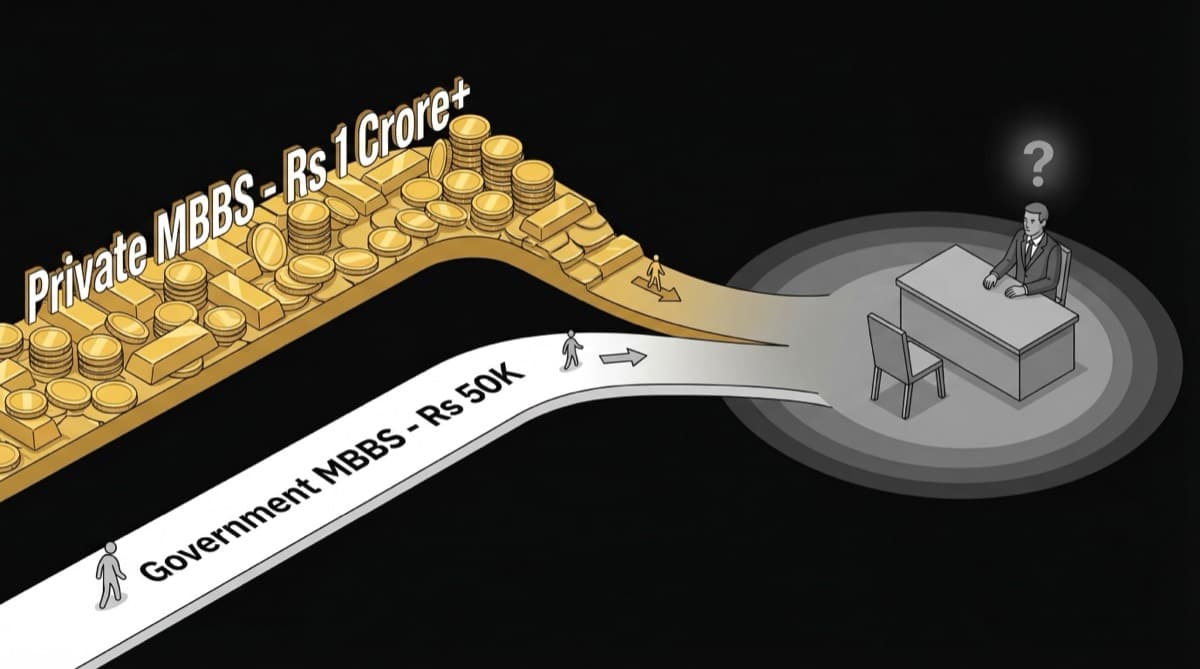

A government medical college MBBS costs Rs 50,000/year. A private deemed university MBBS costs Rs 25 lakhs/year. That's a 50x cost difference for the same degree, the same curriculum, the same examination, and — critically — the same job market. The doctor who paid Rs 1 crore for medical college and the one who paid Rs 3 lakhs compete for identical positions at identical salaries. This isn't a quirk of the system — it's a structural inequality created by capitation fee economics, seat scarcity, and the absence of meaningful fee regulation.

How Large Is the Cost Disparity Between Government and Private Medical College?

The gap is staggering. Annual MBBS fees | Rs 10,000-1,00,000 | Rs 10-25 lakhs | Rs 15-30 lakhs Total MBBS cost (5.5 years) | Rs 50,000-5 lakhs | Rs 55 lakhs-1.4 crore | Rs 80 lakhs-1.65 crore Selection criteria | NEET rank (top 40%) | NEET rank (lower brackets) + fee capacity | NEET rank + fee capacity Teaching hospital volume | High (government hospitals have massive patient loads) | Variable | Variable Faculty quality | Generally experienced (government employment attracts senior academics) | Variable | Variable Post-MBBS starting salary | Rs 40,000-90,000/month | Rs 40,000-90,000/month | Rs 40,000-90,000/month Degree recognition | MCI/NMC recognized | MCI/NMC recognized | MCI/NMC recognized

The bottom line: The starting salary column is identical. A hospital hiring a junior doctor doesn't pay more because the candidate attended a costlier college. The degree is the same. The license is the same. The market doesn't differentiate.

Why Doesn't the Job Market Reward the Higher Investment in Private Medical College?

Three structural factors explain this. Same Degree, Same Exam, Same License

Every MBBS graduate — government or private — sits for the same NMC licensing examination and receives the same registration. Employers don't (and legally can't) distinguish between graduates based on college type. The degree is "MBBS" — there's no "MBBS (Government)" or "MBBS (Private)" distinction on the certificate.

Employer-Driven Market

When hospitals hire junior doctors, they select based on: clinical competence, personality fit, willingness to accept offered salary, and availability. College brand matters for PG entrance (marginally) but not for employment. A corporate hospital chain filling 50 junior doctor positions doesn't sort applications by college fee level.

Supply Overwhelms Differentiation

With 1,18,000 MBBS graduates annually, the supply of qualified doctors exceeds demand at every salary point. In this market, the distinguishing factor isn't where you studied — it's whether you're willing to accept the offered terms. A private college graduate carrying Rs 1 crore in debt may actually be more desperate to accept low-paying positions, not less.

What Are the Structural Economics Behind Medical College Capitation Fees?

Why Private Colleges Charge What They Charge

Private medical colleges are businesses. Their revenue model depends on:

- Capitation fees / management quota fees: The primary revenue source. Seats sold at Rs 10-25 lakhs/year generate Rs 50-200 crore in annual fee revenue for a 150-seat college

- Hospital revenue: The teaching hospital generates clinical revenue from patients

- Government incentives: Land grants, tax benefits, and recognition fees

The fees are set at the maximum the market will bear — which is determined by one factor: the desperation of students who didn't score high enough for government seats.

Why Students Pay Despite the Poor ROI

Seat scarcity creates desperation. India has approximately 47,000 government MBBS seats and 71,000 private seats. A student ranked in the top 40% of NEET gets a government seat. Everyone else faces a choice: pay private college fees or abandon medicine entirely.

Parental aspiration drives decisions. In many Indian families, "my child is a doctor" carries social capital that overrides financial calculation. Parents take loans, sell property, and exhaust savings to fund private medical college — often without understanding the ROI implications.

Information asymmetry is extreme. Most families don't calculate the lifetime ROI comparison between government and private medical education. They see the degree as the goal, not the financial architecture of the career it leads to.

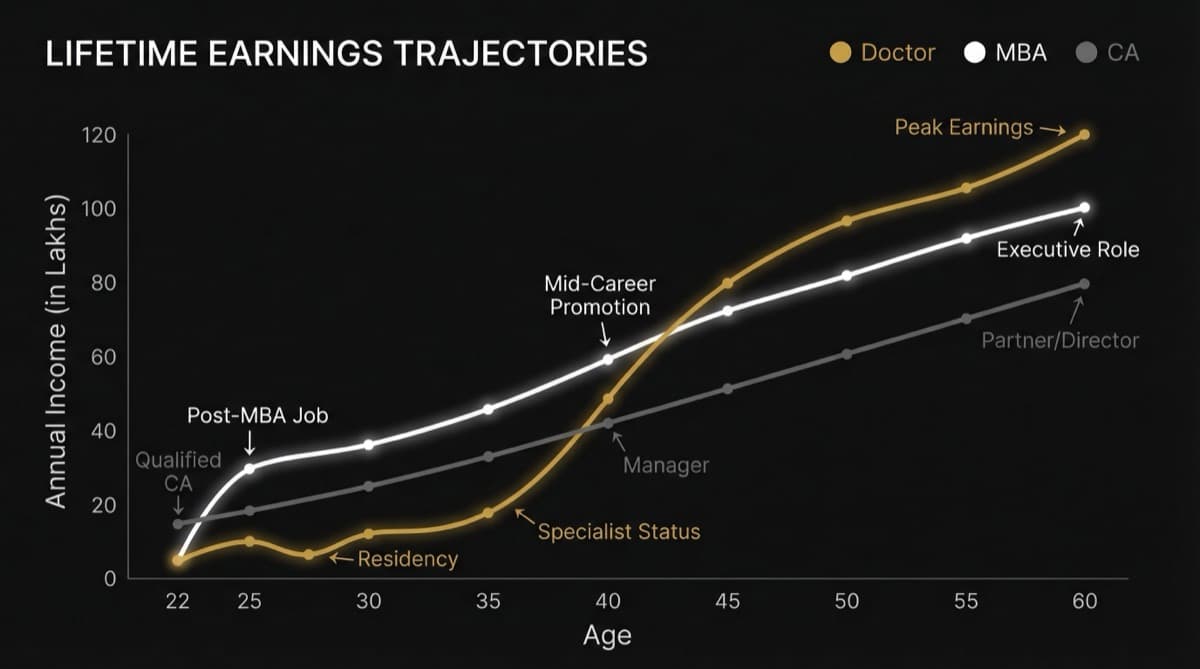

How Does the Debt Burden Diverge Between Government and Private Graduates?

The financial trajectories are starkly different. Education loan | Rs 0-5 lakhs (if any) | Rs 40-80 lakhs Monthly EMI (10-year repayment) | Rs 0-6,000 | Rs 50,000-1,00,000 Starting salary | Rs 50,000-90,000/month | Rs 50,000-90,000/month Net income after EMI | Rs 50,000-90,000 | Rs 0-40,000 Years to debt freedom | 0-3 years | 10-15 years Ability to invest/save at age 25 | High | Near zero Ability to take career risks | High | Very low (debt constrains choices)

The compound effect: The government college graduate starts investing at 25. The private college graduate starts investing at 35-38 (after clearing debt). Over a 30-year investment horizon, this 10-year gap creates a wealth difference of Rs 1-3 crore through compounding alone — on top of the Rs 1 crore already spent on fees.

What Two-Track System Does This Cost Disparity Create?

The cost difference creates two fundamentally different career paths. Track 1: Government College Graduates (Financial Freedom)

- Enter the workforce debt-free or with minimal debt

- Can choose based on interest, not financial desperation

- Can afford to prepare for NEET PG without time pressure

- Can take lower-paying but educationally valuable positions

- Can invest from day one of earning

- Have the financial runway to start clinics or practices later

Track 2: Private College Graduates (Debt Trap)

- Enter the workforce carrying Rs 50-80 lakhs in debt

- Must accept the first available job to service EMIs

- May skip PG preparation to earn immediately

- Cannot afford low-paying fellowship or academic positions

- Cannot invest during the critical early-career compounding years

- Financial pressure limits career choices for 10-15 years

The irony: The student who paid more for medical education has fewer career options, not more. Debt constrains the very flexibility that building a successful medical career requires.

Frequently Asked Questions

Is paying for a private medical seat worth it? Purely on financial ROI: usually not. The lifetime earnings of a private college graduate and a government college graduate are essentially identical — same salary ranges, same career trajectory. The private college graduate just starts with Rs 50-80 lakhs more debt. The seat is only "worth it" if the alternative is not becoming a doctor at all — and if you've calculated the debt burden honestly.

Do private medical college graduates earn less than government college graduates? No — there is no salary differential based on college type for the same qualifications. The market pays for the degree and clinical competence, not the fee structure of the institution. However, private graduates have lower net income for 10-15 years due to loan repayment.

Why doesn't the government regulate private medical college fees? Fee regulation exists in some states through fee regulatory committees, but enforcement is inconsistent. Private colleges lobby against fee caps, argue that higher fees are needed for infrastructure investment, and use legal challenges to delay regulatory action. Some colleges also charge "donations" or "management quota fees" that fall outside fee regulation frameworks.

Should I take a bank loan for private medical college? Only if you've done the full ROI calculation: total cost including interest, monthly EMI burden during early career, comparison of net income (after EMI) with non-medical career alternatives, and timeline to debt freedom. Many families take these loans without this analysis and face financial distress later.

How can the system be made fairer? Three structural interventions: (1) Expand government medical seats to reduce the proportion of students forced into private colleges, (2) Enforce meaningful fee regulation across all private medical colleges, (3) Create income-contingent loan repayment programs (like the UK or Australia) where EMIs adjust based on actual income.

futurise. builds premium healthcare brands in 48 hours. Learn more at futurise.studio