On this page

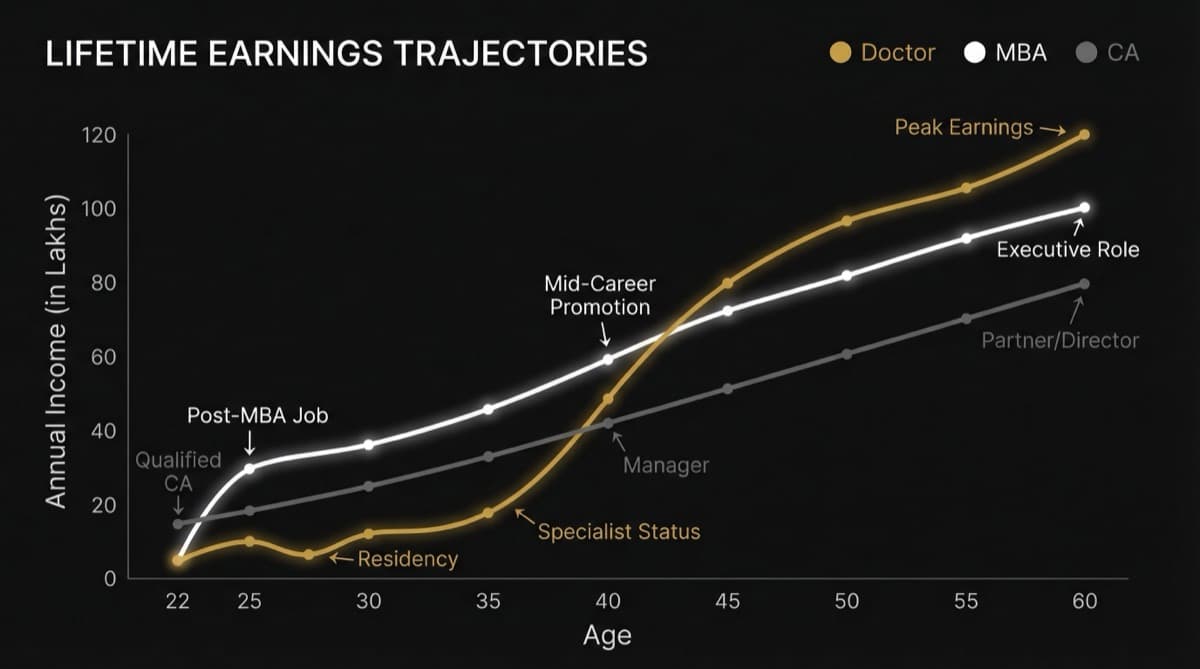

The Income Gap Nobody Talks About

A Dermatologist in Mumbai earns Rs 12-20L monthly from clinic. An Internal Medicine doctor in the same city earns Rs 3-4L. Same city. Same education duration. Different economics. The difference isn't the doctor—it's who pays and how much they pay.

When your patient pulls out a credit card instead of an insurance claim form, your income multiplies. Dermatology and Cosmetic Surgery win because self-pay patients fund premium pricing. Internal Medicine loses because insurance companies set the price. That's the structural gap.

Q.What Is Structural Mechanism 1: Payment Source Determines Income Ceiling?

| Specialty | Primary Payment Source | Insurance Company Controls Price? | Patient Direct Pay % | Average Consultation Fee | Income Model |

|---|---|---|---|---|---|

| Dermatology | Self-pay + Corporate accounts | 8-12% | 88-92% | Rs 800-2,500 | Margin-based (high volume + high fee) |

| Cosmetic Surgery | Self-pay exclusively | 0% | 98-100% | Rs 10,000-50,000+ | Luxury (low volume + premium price) |

| Aesthetic Medicine | Self-pay exclusively | 0% | 99%+ | Rs 5,000-15,000 | Membership + retail (repeat treatments) |

| Gynecology | Insurance + self-pay | 35-45% | 55-65% | Rs 500-1,500 | Volume-based (split income model) |

| Ophthalmology | Insurance + self-pay | 40-50% | 50-60% | Rs 300-1,000 | Volume-split (insurance caps ceiling) |

| Internal Medicine | Insurance-dependent | 80-90% | 10-20% | Rs 200-500 | Insurance grid (price ceiling set by IRDA/TPAs) |

| Pediatrics | Insurance + self-pay | 50-60% | 40-50% | Rs 300-800 | Volume-dependent (insurance limit blocks growth) |

| Orthopedics | Insurance + self-pay + workers comp | 45-55% | 45-55% | Rs 800-2,000 | Surgery-dependent (insurance caps non-surgical consults) |

What you're reading: Dermatology's 88-92% self-pay percentage means an insurance company controls only 8-12% of your fee structure. When patient volume increases by 20%, your income increases by 20%. For Internal Medicine, if insurance companies control 80-90% of your fees, and TPA (Third-Party Administrator) rates are capped at Rs 200-300 per consultation, you can't raise your fee. You can only raise volume—and volume is finite.

Q.What Is Structural Mechanism 2: Insurance Company Fee Caps (2026 Data)?

| Specialty | IRDA / TPA Average Approved Fee | Max Monthly Cap Per Doctor | How Insurance Companies Block Growth |

|---|---|---|---|

| Internal Medicine (Metro) | Rs 150-250 | Rs 1,50,000-2,00,000 | Consultation capped; patients referred to network; doctors reduced to appointment capacity |

| General Practice | Rs 100-150 | Rs 80,000-1,20,000 | Lowest tier; insurance directs to cheaper physicians |

| Gynecology (routine) | Rs 200-350 | Rs 2,00,000-2,80,000 | Surgery fees allowed, consult fees capped; surgical procedures inflate actual income |

| Orthopedics (routine) | Rs 250-400 | Rs 2,50,000-3,20,000 | Similar: surgery lifts income, consultation capped |

| Cardiology (routine) | Rs 300-500 | Rs 3,00,000-4,00,000 | Intervention lifts income; routine consults undercompensated |

| Dermatology (insurance) | Rs 500-800 | Rs 5,00,000-6,00,000 | Dermatology charges more but patients avoid insurance; self-pay bypasses caps |

| Plastic/Cosmetic Surgery | Not typically covered | Unlimited (self-pay) | Insurance exclusion = price freedom |

Reading this table: Insurance companies approve an Internal Medicine consultation at Rs 150-250. If you see 40 patients daily (8-hour clinic), that's Rs 6,000-10,000 daily, Rs 1,50,000-2,00,000 monthly. That's your ceiling unless you add procedures. A Dermatologist seeing the same 40 patients at Rs 800-2,500 (self-pay) earns Rs 32,000-1,00,000 daily. The insurance company created a 5-8x income gap without changing the actual work.

Q.What Is Structural Mechanism 3: Dermatology's Economic Model—Why It Works?

| Revenue Stream | % of Income | Mechanism | Growth Rate |

|---|---|---|---|

| Cosmetic Procedures (fillers, botox, laser) | 45-55% | High margin (Rs 3,000-15,000 per 20-min procedure), low cost per procedure (material cost 5-10%), repeat customers | +18-22% annually |

| Prescription + Retail (skin care products) | 15-20% | Clinic retails branded skincare; 25-40% markup; repeat purchase every 30-45 days | +12-15% annually |

| General Dermatology (conditions, treatments) | 20-25% | Consultation + treatment; insurance covers 8-12% of these; patient pays 88-92% | +2-5% annually |

| Membership/Retainer Programs | 5-8% | Annual membership Rs 15,000-30,000; quarterly facials, consultations, skincare; recurring revenue | +25-30% annually |

| Subspecialty Certifications (Trichology, Laser, Aesthetics) | 3-5% | Premium positioning; Rs 2,000-5,000 per consult premium; builds moat | +8-12% annually |

What this means: A Dermatologist doesn't live or die by consultation volume. A Dermatologist earns on repeated procedures, prescription sales, and membership retention. A single patient on membership + quarterly laser treatments generates Rs 40,000-80,000 annually (compared to Rs 1,000-2,000 from general dermatology consults for Internal Medicine scale). This economic model compounds monthly.

Need help with this?

Our team specializes in healthcare branding. Get personalized advice in a free 15-minute call.

Book a free 15-minute callQ.What Is Structural Mechanism 4: Internal Medicine—Why Income Stagnates?

| Revenue Stream | % of Income | Constraint | Ceiling |

|---|---|---|---|

| Outpatient Consultation | 70-75% | Insurance cap + patient volume finite | Rs 1,50,000-2,00,000/month |

| IPD (Inpatient) | 15-20% | Hospital controls bed allocation + insurance length-of-stay limits | Rs 50,000-80,000/month |

| Procedures (minimal in IM) | 3-5% | Internal Medicine has no high-margin procedures; endoscopy/biopsy referred out | Rs 10,000-20,000/month |

| Retainer Contracts (corporate) | 2-5% | Few corporates contract IM docs; mostly for routine employee health checks | Rs 20,000-50,000/month |

| Retail/Prescription Revenue | 0-2% | Doctors don't retain retail rights; pharmacy separated by law | Negligible |

Reading this: Internal Medicine income is 100% dependent on patient volume, insurance fee caps, and hospital allocation. No leverage on price (insurance controls it). No recurring revenue model (each patient = one-time event). No high-margin procedures. No retail revenue stream. Income growth requires hiring more patients—but those patients flow through insurance networks controlled by hospital administration and TPAs. A Dermatologist controls their entire income architecture. An Internal Medicine doctor rents their income from insurance companies.

Q.What Is Structural Mechanism 5: Patient Willingness to Pay—The Real Driver?

| Scenario | Dermatology (Cosmetic) | Internal Medicine (Acute) | Difference |

|---|---|---|---|

| Patient has Rs 5,000 | Botox session | 0 consultations (too cheap) | Derm patient pays; IM patient doesn't |

| Patient has Rs 15,000 | 3 facial treatments | 30 consultations (capped by insurance) | Derm captures full amount; IM capped at Rs 200-300 per consult |

| Patient has Rs 50,000 | Filler series (custom) | 100+ consultations (logistically impossible) | Derm converts willingness-to-pay into volume; IM can't absorb it |

| Patient has emergency (heart attack) | N/A | Consult Rs 200 (negotiated down) | Patient pays whatever required; IM doc doesn't benefit (hospital does) |

What you're seeing: Dermatology patients have high willingness to pay (cosmetic procedures aren't "necessary"—they're aspirational). Internal Medicine patients have zero willingness to pay (chest pain requires treatment; they don't choose it). When patient urgency is low but willingness-to-pay is high, the doctor captures pricing power. When patient urgency is high but ability-to-pay is low, the doctor becomes a cost center and insurance negotiates price down.

Q.Why This Gap Is Structural (Not Random)?

Internal Medicine won't boom until one of three things happens:

- 1Insurance companies raise fee approvals for IM consultations to Rs 500-800 (unlikely; insurance is designed to reduce costs)

- 2Internal Medicine doctors start high-margin procedure revenue (impossible; IM is diagnostic, not procedural)

- 3Corporate wellness contracts scale to replace insurance revenue (possible but slow; corporates pay Rs 150-300 per employee checkup)

Dermatology will keep booming because the entire economic model (self-pay + high margin + repeat procedures) is structural. You can't "fix" Internal Medicine's income problem with hard work or better bedside manner. The problem isn't the doctor—it's the payment architecture.

Frequently Asked Questions

Q: So should I avoid Internal Medicine if I want income?

A: Not if you're clear about the trade-off. Internal Medicine in a government hospital pays Rs 1-1.2L monthly and offers lifetime job security + pension. Internal Medicine in a private hospital pays Rs 3-4L monthly and offers no security (you can be replaced). Internal Medicine in corporate retainer contracts pays Rs 5-8L monthly and offers moderate security (contracts renew annually). The salary floor is real, but if you stack retainer contracts + hospital consulting + educational content revenue, you can reach Rs 8-12L monthly. It requires portfolio income, not single-specialty income. Dermatology reaches Rs 12-20L from clinic alone.

Q: Why aren't more Internal Medicine doctors switching to Cosmetic Medicine?

A: Because switching costs are high and structural position matters. A Dermatologist switching to Cosmetics means adding laser equipment (Rs 30-50L capital), learning procedure skills, and rebuilding patient trust in a new specialty. An Internal Medicine doctor has a patient base that trusts them for acute care—that trust doesn't transfer to cosmetic procedures (different patient psychology). The economic model you're born into (in your residency specialty) becomes sticky. You can add revenue streams to Internal Medicine (retainer contracts, content), but you can't easily become Dermatology.

Q: Can I do Internal Medicine + build a Cosmetics side practice?

A: Yes, but you need to separate the brand. If you're known as an Internal Medicine doctor in your network, patients trust you for cardiac issues, not Botox. You'd need to build a separate clinic, separate brand, separate patient base (cosmetics). That requires Rs 15-25L capital and 18-24 months to build patient trust from zero. By the time you're established, you've effectively become a Dermatologist/Cosmetic specialist. This is possible but it's a career pivot, not a side hustle.

Q: Is this why so many IM doctors leave for NRIs or exit the profession?

A: Yes. IM doctors face structural income compression (insurance caps) + highest patient volume (most burnout) + zero leverage on pricing. After 10 years, an IM doctor earns Rs 4-6L monthly in private practice but works 12-hour days, managing 60+ patients. A Dermatologist earns Rs 15-20L monthly in the same city, working 6-8 hour days, managing 20-25 patients. The burnout-to-income ratio is inverted. IM doctors exit because the economics don't justify the work volume. It's not a personality problem—it's a structural incentive problem.

Q: What about Telemedicine for Internal Medicine? Does that change the economics?

A: Telemedicine compresses IM income further. Insurance companies approve telemedicine consultations at Rs 100-150 (lower than in-person). Telemedicine volume increases (you can see 80+ patients daily), but fees drop 30-40%. For Dermatology, telemedicine is less valuable (skin conditions require physical examination), so Dermatologists keep high-fee in-person consultations. Telemedicine favors insurance-dependent specialties by commoditizing them faster. IM doctors should avoid telemedicine unless it's supplementary (retained patient follow-up), not primary.

futurise. builds premium healthcare brands in 48 hours. Learn more at futurise.studio