On this page

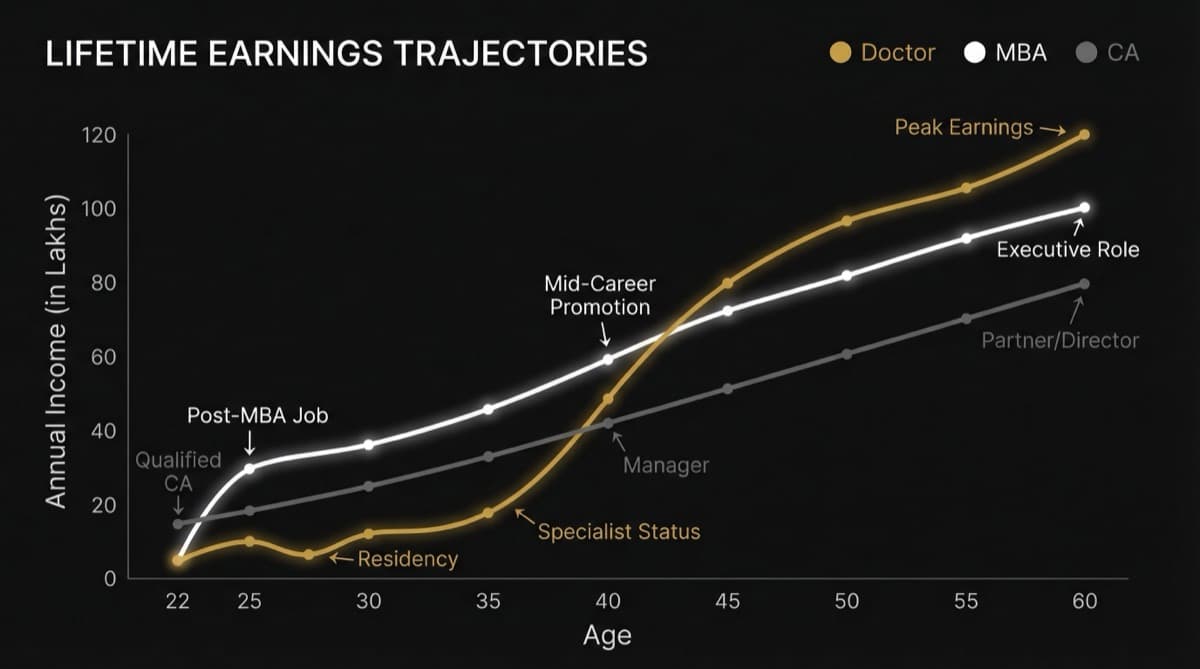

The Income Trap Nobody Sees Until It's Too Late

You've built a clinic that generates Rs 50L annually. You're 45 years old. You have 20 years until retirement. If you save 30% (Rs 15L/year), you'd accumulate Rs 3Cr by age 65. That sounds fine until you do the math: Rs 3Cr at 4% returns = Rs 12L annually (pre-inflation). After 6% inflation, that's Rs 7L real income. You can't retire on Rs 7L/year in a metro. The problem isn't your income—it's that you started saving at 45, your lifestyle inflated with your income, and you invested like a salaried employee instead of a self-employed person.

Most Indian doctors retire with less than Rs 1-2Cr despite earning Rs 30-50L annually for 20+ years. Here's why.

Q.What Is Structural Mechanism 1: The Income-Wealth Paradox (Why High Income ≠ High Wealth)?

| Income Scenario | Annual Income | Spend Rate | Annual Savings | By Age 65 (20 Years) | Real Value (After Inflation) | Retirement Status |

|---|---|---|---|---|---|---|

| Scenario A: Conservative doc (started early, saved 40%) | Rs 40L/year (age 45-65) | Rs 24L/year | Rs 16L/year | Rs 32Cr (compounds at 8%) | Rs 15-18Cr (real) | Comfortable retirement |

| Scenario B: Average doc (late start, saves 25%) | Rs 50L/year (age 45-65) | Rs 37.5L/year | Rs 12.5L/year | Rs 20Cr | Rs 9-11Cr (real) | Tight retirement; need to continue working part-time |

| Scenario C: Lifestyle inflation doc (saves 10%) | Rs 50L/year (age 45-65) | Rs 45L/year | Rs 5L/year | Rs 8Cr | Rs 3.5-4Cr (real) | Below poverty line in retirement; return to work or reduce lifestyle 60% |

| Scenario D: No savings doc (spends 100%) | Rs 50L/year (age 45-65) | Rs 50L/year | Rs 0/year | Rs 0 | Rs 0 | Retirement impossible; continue working until death |

| Scenario E: High earner, late start (Rs 100L/year, saves 20%) | Rs 100L/year (age 50-70) | Rs 80L/year | Rs 20L/year | Rs 40Cr (20 years) | Rs 18-22Cr (real) | Comfortable if worked until 70 |

What you're reading: A doctor earning Rs 50L/year who starts at age 45 and saves 25% ends up with Rs 20Cr nominal (Rs 9-11Cr real). A couple retiring on Rs 9Cr needs 4% yield = Rs 36L annual income. After taxes (30%) and inflation (6%), that's Rs 21L real income. They can't retire on that in a metro (they need Rs 40-50L/year to maintain lifestyle). The problem compounds: late start + low savings rate + lifestyle inflation = retirement disaster.

Q.What Is Structural Mechanism 2: Where the Money Goes (Lifestyle Inflation by Expense Category)?

| Expense Category | Age 30 (Resident) | Age 35 (Early Practice) | Age 40 (Established) | Age 50 (Peak Earnings) | Change |

|---|---|---|---|---|---|

| Housing | Rs 1.5L/year (rent) | Rs 8L/year (mortgage) | Rs 15L/year (larger home mortgage) | Rs 20L/year (metro area, premium locality) | +1233% |

| Education (Kids) | Rs 0 | Rs 5L/year (school) | Rs 10L/year (international school) | Rs 15L/year (IIT coaching + international school) | +∞ (wasn't a cost category, now massive) |

| Travel | Rs 2L/year (domestic, budget) | Rs 4L/year (occasional international) | Rs 8L/year (family travel) | Rs 15L/year (business + family trips, international) | +650% |

| Vehicles | Rs 1.5L/year (used car maintenance) | Rs 4L/year (new car) | Rs 8L/year (premium car) | Rs 15L/year (2 premium cars) | +900% |

| Healthcare (Self) | Rs 1L/year (basic) | Rs 2L/year | Rs 3L/year (preventive care, specialist consults) | Rs 5L/year (diagnostics, specialist care, concierge medicine) | +400% |

| Household Staff & Maintenance | Rs 1L/year (housemaid) | Rs 2L/year (housemaid, driver) | Rs 5L/year (housemaid, driver, maintenance) | Rs 10L/year (housemaid, driver, maintenance, premium help) | +900% |

| Dining & Entertainment | Rs 2L/year | Rs 4L/year | Rs 8L/year | Rs 15L/year (frequent restaurant, clubs, events) | +650% |

| Charitable Giving | Rs 0 | Rs 1L/year | Rs 3L/year | Rs 10L/year (feels obligation to give; peer pressure) | +∞ |

| Insurance & Investments | Rs 0 (no awareness) | Rs 2L/year (basic life insurance) | Rs 3L/year (life insurance only) | Rs 3L/year (stagnant; under-invested relative to income growth) | Flat (missed opportunity) |

| Other (Hobbies, gifts, etc.) | Rs 1L/year | Rs 3L/year | Rs 5L/year | Rs 10L/year | +900% |

| TOTAL ANNUAL EXPENSE | Rs 10.5L | Rs 30L | Rs 60L | Rs 110L | +945% |

| Annual Income | Rs 15L | Rs 40L | Rs 60L | Rs 100L | +567% |

| Savings Rate | 30% | 25% | 0% | -10% (living beyond means) |

What this means: Your expense growth (945%) outpaces income growth (567%). By age 50 earning Rs 100L, you're spending Rs 110L (living beyond means, running deficit). You're borrowing from savings or taking loans. The structural issue: expense inflation compounds (kids' education gets more expensive, housing more expensive, lifestyle expectations locked in). Income scales linearly. By age 50, lifestyle is unsustainable.

Q.What Is Structural Mechanism 3: Why Doctors Invest Poorly (The Insurance Company Trap)?

| Investment Type | What Doctors Choose | Why They Choose It | Returns (Real) | Better Alternative | Return Difference |

|---|---|---|---|---|---|

| Insurance Products (ULIP, endowment) | 30-40% of investable income | Insurance agents (friends, family connections) pitch hard; doctors lack investment literacy; ULIP feels "safer" (insurance + investment) | 3-4% real | Index mutual funds | +4-5% real |

| Real Estate (2nd/3rd property for investment) | 25-30% of investable income | "Property is safe, government won't take it away"; emotional attachment | 4-5% real (if bought at right price; most doctors overpay) | Equity mutual funds | +3-4% real |

| Gold (physical, not ETF) | 10-15% of investable income | Jewelry, weddings, family tradition; no investment literacy; gold feels "real" | 2% real (accounting for storage, insurance) | Equity index funds | +6% real |

| Bank Fixed Deposits | 20-30% of investable income | "FD is safest"; bank staff pitch aggressively; no effort required | 2% real (post-tax, post-inflation) | Equity funds | +6% real |

| Direct Stock Picking | 5-10% (riskier doctors) | Listen to tips from friends; no fundamental analysis; emotional buying/selling | -2% real (underperformance due to poor timing, overconfidence) | Index funds | +6% real |

| Equity Mutual Funds (correct choice) | 5-10% | Correct alternative but doctors underweight because of "stock market risk" | 8-10% real | — | Baseline |

Reading this: Doctors allocate 60-80% of savings to low-return products (insurance, real estate, gold, FDs) while allocating only 5-10% to equity (which has highest returns). The reason: insurance agents leverage social connections (friend/family agent), real estate feels "real," gold is cultural. Equity funds feel risky (they're not; they're just volatile). A doctor investing Rs 15L/year for 20 years at 4% real return ends up with Rs 30Cr real. Same doctor investing at 8% real return ends up with Rs 52Cr real. The difference: Rs 22Cr. That's due to poor asset allocation (not investment skill, just missing the right asset class).

Need help with this?

Our team specializes in healthcare branding. Get personalized advice in a free 15-minute call.

Book a free 15-minute callQ.What Is Structural Mechanism 4: The Tax Trap (Doctor Income + Tax Structure)?

| Scenario | Gross Income | Tax Rate (Combined: Income + ST + GST) | Net Income | Doctor Thinks Net Income Is | Tax Loss |

|---|---|---|---|---|---|

| Salaried Doctor (Rs 50L) | Rs 50L | 42% (IT 30% + surcharge 10% + ST 2%) | Rs 29L | Rs 50L (haven't figured out taxes) | Rs 21L (42% loss) |

| Self-Employed Doctor, No Tax Planning | Rs 50L gross clinical | 45% (IT 30% + surcharge + ST + GST input cost recovery none) | Rs 27.5L | Rs 50L | Rs 22.5L |

| Self-Employed Doctor, Basic Tax Planning (HUF, expense claiming) | Rs 50L gross clinical | 35% (IT 30% + surcharge reduced via HUF structure + expense claims lower taxable income) | Rs 32.5L | Rs 30L (underestimate) | Rs 17.5L |

| Self-Employed Doctor, Advanced Planning (corporation structure, investment strategies) | Rs 50L gross clinical | 25% (effective: IT lower via corporate structure, expense optimization, investment deductions) | Rs 37.5L | Rs 32.5L | Rs 12.5L |

What this means: A doctor earning Rs 50L gross (self-employed) and doing no tax planning ends up with only Rs 27.5L net. They think they're earning Rs 50L and spend Rs 45L (because lifestyle is scaled to gross income, not net income). They end up with negative savings. A doctor with tax planning keeps Rs 37.5L net (additional Rs 10L saved). Over 20 years, that Rs 10L/year compounds to Rs 20Cr additional wealth. Most doctors don't have tax planning; they pay whatever accountant calculates. That's a Rs 20Cr mistake.

Q.What Is Structural Mechanism 5: The Cognitive Blind Spot (Why Doctors Don't See It Coming)?

| Phase | What Doctor Thinks | What's Actually Happening | Warning Sign Ignored |

|---|---|---|---|

| Age 30-35 | "I'm in residency/early practice; once I earn more, I'll save aggressively" | Early years are the MOST important for compound growth (smallest savings grow 30-35 years); lost opportunity | Doctor ignores compound growth value of early savings |

| Age 35-40 | "I'm building practice; expenses are high; I'll save more once practice is stable" | Practice is now stable; but lifestyle locked in at high spend rate; expense inflation hard to reduce | Doctor doesn't adjust spend rate despite stable practice |

| Age 40-45 | "I'm earning well now; I have time to save for retirement" | Only 20 years left; high savings rate now needed to compensate for lost early years; compounding time running out | Doctor underestimates how much they need to save now |

| Age 45-50 | "I'll save Rs 10-15L/year, which should be enough" | Rs 10-15L/year for 15-20 years at 5% real return = Rs 20-25Cr real; needs Rs 30-40Cr to retire comfortably; still behind | Doctor's target savings insufficient due to late start |

| Age 55 | "I have 10 years; I can catch up with aggressive investments" | 10 years of 8-10% returns on Rs 15L/year = Rs 20Cr; still short Rs 15-20Cr; retirement at 65 impossible | Doctor doesn't realize catch-up is too late; no alternative except working longer |

| Age 60+ | "I can't retire; I have to keep working" | Burnout, health issues, income falling (patient volume declining); forced to work with declining returns | Doctor doesn't see the trap until it's inescapable |

What this means: Doctors systematically delay savings because they underestimate compound growth's time value. A doctor at 35 thinks "I have 30 years, plenty of time." They don't realize that waiting until 45 means giving up 10 years of compound growth (that Rs 10 years compounds to Rs 20-30Cr by age 65). The cognitive blind spot is underestimating early-year compounding and underestimating how fast the final 20 years of career approach.

Frequently Asked Questions

Q: At age 40, earning Rs 50L/year, what's my realistic retirement target?

A: If you save Rs 15L/year (30% savings rate) for 25 years (age 40-65) at 7% real returns, you'll have Rs 65Cr real value. That generates Rs 2.6Cr income annually (4% yield), minus taxes (25%), = Rs 1.95Cr after-tax = Rs 16L monthly. You can retire on that in a metro (assuming Rs 15-20L/year lifestyle). If you save only Rs 7.5L/year (15% savings rate), you'll have Rs 32Cr real = Rs 1.3Cr income = Rs 10L monthly after-tax. That's tight. Target: start saving 30% immediately. If you haven't, increase to 35-40% NOW.

Q: Should I invest in a 2nd property as retirement corpus?

A: Only if real estate appreciates >6% annually (after accounting for property taxes, maintenance, vacancy periods). In most Indian metros, real estate appreciates 4-5% (Delhi, Mumbai) or even negative real (Tier-2 cities). Equity mutual funds return 8-10% real reliably. Rs 30L invested in property at 4% real growth = Rs 60Cr by age 65. Same Rs 30L invested in equity at 8% real growth = Rs 120Cr by age 65. Property is a lifestyle choice (you live there) or a poor investment (low returns). For pure return, equity wins. For peace of mind, property might win (physical asset). Choose based on actual returns, not emotion.

Q: What's the minimum annual savings target for doctors?

A: (Desired Annual Retirement Income × 25) - Current Investments. If you want Rs 30L/year in retirement and have Rs 0 saved at age 40, minimum target = Rs 75L annual savings to build Rs 30Cr by 65. If you want Rs 20L/year (comfortable living), target = Rs 50L annual savings. Most doctors earning Rs 50L can't save Rs 50L annually (expense inflation prevents it). Reality: save 30-40% of income starting now, adjust expectations down, or plan to work until 70. Pick one.

Q: Is hiring a financial advisor worth it?

A: Yes, if you have >Rs 1Cr invested and >Rs 10L/year savings. Cost: Rs 50-100K/year or 0.5-1% of AUM (assets under management). Expected value: advisor saves 3-5% annually through tax optimization, asset allocation, behavior correction (preventing emotional selling). On Rs 1Cr, 3% return improvement = Rs 3L extra annually; advisor cost Rs 50K = 1600% ROI. For doctors with complex income (clinical + advisory + equity) and high investable assets, advisor is worth it. For doctors with simple income and no tax planning, advisor might save even more (5-10% from tax planning alone).

futurise. builds premium healthcare brands in 48 hours. Learn more at futurise.studio